Whole Life Insurance for Dummies | Top Whole Life

WHOLE LIFE INSURANCE FOR DUMMIES

STOP! Don't buy Whole Life before reading this!

Before reading this article, do not even think about requesting information about whole life insurance.

Life insurance is an excellent decision for your financial future. However, be careful before you start requesting quotes, as this could open up the floodgates of agents who will begin to call you. As these agents call, they will bombard you with information you do not understand. We find this ultimately discourages you from moving any further. We want to make sure you are ready to receive calls about your life insurance to get the coverage you need.

This article will go over the top five things you must know about whole life insurance.

- Understanding Whole Life Insurance

- Reasons To Purchase A Whole Life

- Using A Whole Life Policy

- Picking The Right Whole Life

- The Process Of Purchase

Whole Life Insurance for Dummies article will be your guide to making the best decision possible as you search for a life insurance policy. Whether you want term insurance or permanent coverage, this article will help direct you to the right option. Much of this information is overwhelming, but you will feel confident speaking with agents, obtaining quotes, and locking in coverage after reviewing this article.

1. Understanding Whole Life Insurance

Whole life insurance is the original insurance. When insurance started, all that existed was whole life. Understanding whole life insurance is not as difficult as it may seem.

However, make sure to educate yourself about the different types of life insurance available to you. There are several different types of insurance policies that may fit your needs, such as the ones below:

Different types of life insurance policies:

- Whole Life Insurance

- Term Life Insurance

- Variable Life Insurance

- Indexed Universal Life Insurance

- Universal Life Insurance

- Guaranteed Issue Life Insurance

- Accidental Death Insurance

So many different choices

Here are the differences and how they work:

Whole Life Insurance

Whole life insurance, referred to as "permanent insurance," is the most straightforward option. Whole Life Insurance policies have a level premium; they accumulate a guaranteed cash value each year, and the death benefit is whole life insurance a guaranteed death benefit. Additionally, the beneficiaries would receive the death benefit tax-free if you were to pass away.

As a result of the guarantees, whole life typically has a whole life insurance faqs much whole life insurance cost to the policy owner.

The Mortgage Analogy

A whole life policy is very similar to how your home mortgage works. When you purchase a home, let's say for $200,000, you commit to paying a monthly mortgage payment. This monthly mortgage payment is just like a whole life insurance premium. In the beginning, the premiums seem very costly because you are paying down mostly interest on the loan.

The same will hold with your Whole life policy. You will be paying your premiums in the early years, and there will seem to be very little in your cash value savings account.

Not to worry, just like with your mortgage, over time, you will see the equity continue to grow!

Whole life has one big upside compared to your mortgage; you have asset protection in the way of your death benefit.

Term Life Insurance

Term insurance provides pure death benefit protection for a specific time. Term insurance can be purchased in 10, 15, 20, or 30 years blocks. During the term insurance block, the policy will have a set premium. Therefore, term insurance is the cheapest choice regarding the premium cost when searching for an insurance policy.

Think of term insurance as "renting" you're insurance. So when you buy term, you are essentially renting that $200,000 home we referenced in the above whole life description for some time.

Like Renting

Now, don't get me wrong, I am not trying to put down anyone reading that renting is a bad option. On the contrary, renting is an excellent option for many people. Term insurance is very popular with so many people as if it offers the protection needed at a fraction of the cost. However, you will want to keep in mind that not all Term insurance policies are created equal.

Some policies are fundamental, and some come with add-ons.

Think of this as renting a home with no furniture or renting a home fully furnished. It will be more costly to rent a home fully furnished with all the bells and whistles. For this reason, term insurance with all the bells and whistles is more costly than others.

Additional Resources: convert term to whole life

Universal Life Insurance

Universal Life Insurance (UL) is most well-known for its flexibility. The flexibility of a UL is a major selling point for this type of policy. Universal life policies have premium payments that are adjustable during the contract's life. So as long as you meet a minimum amount to keep the contract in force, your death benefit stays the same.

On the flip side, if you fall into a large sum of cash and want to build up the cash value account, you could add additional funds to the policy.

A universal policy is like a permanent term insurance policy. The cash value account is used for leverage, just like a whole life's policy cash value may be. But instead, it is there to keep your premiums as level as possible over the lifetime of the contract.

You can read further here: whole life insurance vs universal life insurance

Universal life can be a good choice for permanent coverage. Especially if you chose a Guaranteed Universal Life policy.

Variable Universal Life Insurance

Variable Universal life insurance is a universal life insurance policy with an investment component. This investment component lets you allocate your cash value to stocks and bonds. If you are a risk-taker, then variable life insurance could be attractive if you want to maximize your cash value.

When considering a variable life insurance policy, it would be wise to speak with a Fee-only financial advisor or have a strong understanding of the market. Many who look into life insurance are looking to find ways to avoid risk, so make sure you know this type of insurance.

Variable Rate

Think of this as purchasing a home with a variable loan rate mortgage. Sure, your mortgage interest rates could stay low, but you also expose yourself to the potential for more risk if interest rates were to rise. In addition, if your premiums were to increase, this could create major financial issues, potentially leading to default in the future.

Additional reading: whole life insurance vs variable universal life vule.

Indexed Universal Life Insurance

Index universal life insurance is another Whole life alternative. This policy also has an investment component letting you allocate up to 100% of your cash value to a stock market index, such as the S&P 500 or Nasdaq 100. If the index sees positive growth, the cash value grows, although there is a cap.

Even if the index has negative returns, you will not lose cash value in your policy. Therefore, indexed universal life is a prevalent option. Moreover, index universal life offers many upsides that a variable life policy offers without many risks.

Check out this article: whole life vs indexed universal life iul

Guaranteed Issue Life Insurance

Guaranteed issue life insurance provides coverage without completing any medical underwriting. If you need life insurance and do not want to jump through any hoops, this type of insurance is a great option. The insurance companies will not deny the applicants' insurance as long as they pay their premiums.

Since the insurance company takes on more risk without fully underwriting the insured, the insurance premiums are typically higher. Some guaranteed issue policies have graded benefit or return of premium clauses. Take note of this!

Graded benefits would not pay a full benefit if the insured died two years into the policy. Usually, there is a return of premiums paid as the benefit.

Accidental Death Insurance

Accidental Death Insurance benefits an insured's beneficiaries in the event of a death or partial/complete dismemberment that resulted from a covered accident. These policies will payout and any other coverages that the insured may have in force, such as personal disability coverage and work-provided insurance.

Coverages are typical between $20,000 to $500,000 and are on an individual policy or sold through an employer's benefits offerings. If death were to occur due to an accident, a benefit would be paid in full.

Many policies also pay out if there is a dismemberment incident.

2. Reasons To Purchase A Whole Life Insurance

Knowing what you know about the different insurance options, it is time to consider a simple question.

Why are you considering buying whole life insurance?

Most people buy whole life insurance for two reasons: Cash Value or Death Benefit.

These are very different reasons to purchase whole life insurance, but let's start with death benefit as this applies to any life insurance.

Death Benefit Protection

If you buy whole life insurance for the death benefit protection, whole life insurance may not be the proper fit. You will want to clarify this to your agent when you start calling around. Depending on your personal needs and health situation, you will want to look at a Universal Life Insurance or Term Life Insurance policy.

The following formula is a safe way to calculate your insurance needs when buying for Death Benefit Protection Only:

DIE Formula

In reality, we need to determine just how much life insurance you will need, not just whole life, but any type.

Deciding on an amount can be a tough question to answer, and you must look at your situation and ask yourself some questions. The following formula can help. Also, we have an article that can help you: much whole life insurance need

Debt Protection

First, put together a list of all of your debts. Debts will include all items you feel need to be covered. The most common are items like (Mortgage, Student Loans, Car Loans, Credit Cards, etc.). Next, you will want to add up all the debt you still owe. For example:

Mortgage debt: $200,000

Student Loan: $52,000

Car Loan: $28,000

Credit Card's $10,000

Total - $290,000

Income Replacement

Next, you will want to calculate how much income will be needed to replace what you make for your family. Why is income replacement essential? For example, if you were to pass away and only leave enough to cover your debts, would this leave your family in a situation where they could survive without your income as well?

If you have ever experienced a loss in your family, it can be challenging to get back into the workforce after such a traumatic event. Additionally, if you have kids and a parent dies, this can lead to additional costs like daycare to allow the other spouse to return to work.

How Much Insurance, Then?

Pro Tip: Think about all the things you pay for with your income. It is complicated to figure out how much life insurance you need unless you have a good snapshot of what you need to live. If you want a simple way to find this out, print a bank statement or use an app like MINT.com to figure out your monthly budget.

Let's assume you review your budget, and every month you $3,500. So the income you need to replace is $42,000/year. Now that you know this information, we can plug it into our calculations.

With a Life Insurance Benefit of $1,000,000 tax-free. The policy's death benefit could be used to create an investment income stream.

For example: $1,000,000 earning 6% = $60,000 / Year

After paying UNCLE SAM (Taxes), the take-home income is approximately $40,000.

The above example illustrates how much protection is needed to produce income for a family. The amount required can change drastically depending on your age and personal situation.

For example, if you are in your thirties with one spouse earning $120,000 and the other spouse stays at home watching two kids aged 4 and 2.

You would need to purchase at least $3,000,000 of coverage to replace your income of $120,000 after taxes.

Death Benefit = Income

$1,000,000 = $40,000

$2,000,000 = $80,000

$3,000,000 = $120,000

Pro Tip:

A Whole life policy blended with a term rider is a great option if you want to buy enough insurance to cover income and have a Whole Life policy. Term Insurance Riders will allow you to obtain the benefit amount you need at a fraction of the cost.

Education

Lastly, you will want to calculate and plan to take care of any education expenses incurred in the future if you were to pass.

Do you want to prepare for public high school or private high school? Public College or Private college? Ultimately you will need to decide the right amount for your situation.

Estimates from Collegedata (collegedata.com) say that the average cost of tuition and fees for 2017-18 is about $34,740 for a private college. Also, $9,970 for state residents at public colleges and $25,620 for out-of-state residents attending a public college.

So depending on your wishes, you may want to plan for at least $40k - $140,000 per child. Many of our clients like to use a whole life for college savings; here is an article: whole life insurance kids.

Cash Value or Buying Whole Life As An Investment?

If you are buying life insurance as an "investment," then the above DIE formula will not help you find a design that will meet your expectations.

Whole life insurance has some very desirable features. Still, to have a policy that will offer you high performance and the ability to leverage your cash, these specialty policies cannot be purchased off the shelf like at Walmart or on Amazon (Potentially someday).

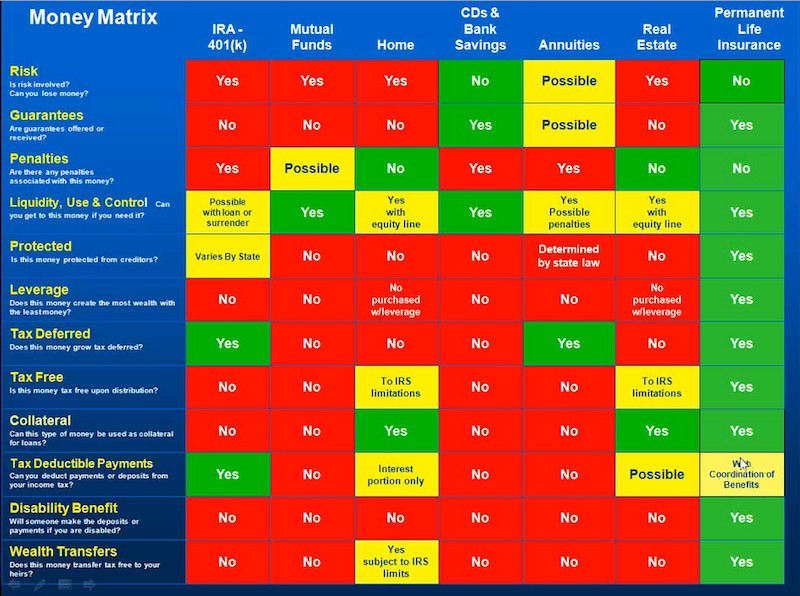

For starters, look at all the benefits of permanent life insurance over other investment options.

Money Matrix Source Money Matrix 2 (debtdiagnosis.com). In general, whole life can be a great source of retirement income if used properly. You can read more: whole life insurance for income.

Top 3 considerations when buying whole life as an investment?

In reality, we cannot discuss how the cash value works without understanding the purpose of the insurance.

3. Using A Whole Life Insurance

Many books have been written about the benefits of whole life insurance, like: "bank on yourself review" and "infinite banking review." But let's quickly review how to use a whole life.

How Do You Want To Use Your Whole Life Insurance?

How you would like to use your cash value life insurance could drastically change what design you will pick.

- Do you want to use it to buy real estate?

- Are you looking to use it to supplement retirement?

- Do you want it for business opportunities?

- Do you want it for education savings?

- Maybe you want it for a vacation?

Regardless of why you want to have whole life insurance, each of these objectives will have a design best suited for it.

How Much Can You Save Per Month?

Whole life insurance is not for everyone. If you do not have low-performing assets or can save, then whole life insurance as an investment tool may not be the best starting point.

However, if you have excess cash, how much of it can you afford to save on a tax-deferred basis? $100, $500, $1000, $2000 per month?

Would you like to save a significant sum upfront and only have to fund your policy for a few years after with a smaller premium? Would you wish only to make one premium payment? All of these are options!

When looking for life insurance as an "investment," the primary concern is the cash value, not the death benefit amount.

Remember that depending on what you want to accomplish, you may need a substantial death benefit to prevent your policy from hitting a MEC limit and becoming a modified endowment contract. If a contract MEC'S, you will lose many of the whole life insurance tax benefits.

How Soon Would You Like To Access Your Cash Value?

Timing is everything, and with whole life insurance, it is no different. When you plan to access your cash values, the time you would like to do so can make a larger difference in the policy design.

- Will you access your high early cash value?

- Do you want to access your cash value in years 10 -20?

- Do you want to access cash value at age 65?

Once you clearly understand your investment objectives, you are halfway there. Then you need to know how you would like to use your cash value life insurance. Precise information about your intentions can help an agent guide you to the proper whole life plan.

Feel free to reach out to one of our Top Whole Life agents. Our life insurance experts can help put together the best policy design.

4. Picking The Right Whole Life Insurance

Compare

Once you know the amount of coverage to buy, start looking at specific life insurance policies.

It's good to keep a few things in mind while you're shopping:

- First, be careful to enter your information on every site you check out. There are many sites that, after entering your information, agents will start to reach out to, and many have high-pressure sales tactics.

- The whole life insurance faqs much whole life insurance cost can be very different for nearly identical policies. When shopping for whole life insurance, especially with an "investment focus," you need to make sure you are working with someone who has experience with custom-designed policies. Don't settle for the first quote you receive; reach out to multiple brokers. Once you start talking to numerous agents, you will want to ask questions to understand the differences to pick the best policy.

- Do not go for the cheapest policy. An affordable premium isn't the best pick all the time. You will need to consider company strength, cash value growth, and past performance.

- You need to get quotes with your health ratings. If you are overweight or whole life insurance for smokers, your prices and cash value will differ from someone who doesn't.

5. The Process Of Purchase

We will go over what to expect from the application process.

Total Application Time

Typically 3-5 Weeks

From start to finish, the entire application process generally takes 3-5 weeks. However, this process can sometimes be shorter, especially today, with algorithmic underwriting.

We have seen clients approved in 3-7 days! However, we have seen clients take much longer to be approved. The most common cause of longer processing times is an applicant with a complex health history.

There have been times when information is needed from a doctor. Obtaining Dr reports can take 30+ days or more, which delays the whole process.

Application

15--30 €‹min

What to expect

- Fill out an application covering basic info and job details. (This can be done over the phone or sent to you via email and scanned back.)

- Be ready to provide your Driver's license, income documentation, and employment data.

- Once you have completed all the information, you need to sign (E-sign or wet signature) to start the process.

Medical Exam

This option doesn't apply if you picked a non-medial whole life. What to expect from your medical exam:

- A nurse will come to you.

- The nurse will measure your height, weight, blood pressure, and pulse.

- Then you will need to give a blood sample and urine sample.

30--45 €‹min

Pro Tip:

- Schedule the exam early in the morning.

- 24 hours before the exam

- Avoid caffeine, sugar, and alcohol.

- Avoid over-the-counter drugs as they might interfere with your test results.

- 6-8 hours before the exam

- Don't eat anything else until you've completed the exam.

- Don't engage in any strenuous exercise.

- 1 hour before the exam

- Drink a glass of water to help ensure you'll be able to provide a urine sample.

Phone Interview

What to expect

- An insurance representative will call you, as scheduled, to ask about your lifestyle (e.g., travel & hobbies) and health history.

- Your broker should provide a list of the questions beforehand to know what to expect.

- Have your primary care physician's name, address, and phone number handy.

20--25 €‹min

Underwriting and Approval

What to expect

- If all looks good with your medical exam and phone interview, you should hear from your agent quickly.

- If things don't look perfect, there is a chance that the insurer may contact you to ask for more information. This would extend the underwriting time.

- Once a final decision has been reached, your agent will reach out with the news. You will want to review the offer and sign a delivery receipt if it is in line with your wishes. Then authorize the payment method to activate the policy.

- Just remember being approved for a life insurance policy is not guaranteed. So any offer from an insurance company is a good offer. However, if you feel like something does not match up and you should have had better underwriting, your agent should reach out and fight for you. Mistakes are made, and fighting for the best rate can be worth thousands!

2-4 weeks

Policy Goes Into Effect

What to expect

- Once your application is approved, the insurer will notify you and request payment. You get a paper or electronic policy, a certificate of proof that your policy is in effect.

- Store your policy and a copy of your application with your other important documents. This way, you'll be able to reference it in the future. You should also ensure your beneficiary knows about the policy and has access to it.

And that's the whole process from start to finish!

Check out:

techonology changing online whole life insurance quote

buying whole life insurance while pregnant

whole life insurance for cancer survivors

Final Word

So as you learned what whole life insurance is, how to use it, and how to choose the right one for you.

Once you understand what you are looking for, your decision is easy.

If all you want now is a quote, you can get one here: single whole life quote.

If you wish to help pick the best whole life, try this article: top 7 whole life insurance companies for cash value.

Leave us a comment: Are you looking for Cash Value or Death Benefit?