Whole Life Insurance Dividend Rate History [2026 Update]

Updated June 7, 2026

Whole Life Insurance Dividend Rate History Chart

Use the chart above for a visual snapshot of how major mutual carriers compare on dividend interest rates (DIR). The tables below add year-by-year detail, 2026 announcements, and carrier-specific history for long-tail searches (e.g. Mass Mutual dividend rate history, New York Life dividend rate history).

Whole life insurance historical performance and charts with expert analysis. We have an updated list of Whole Life Insurance Dividend History.

We also go back to give you average rates for the past 5, 10, 15, and 20 years. This can help you understand where each company ranks historically. We use all this data to get our seven top 7 whole life insurance companies for cash value every year.

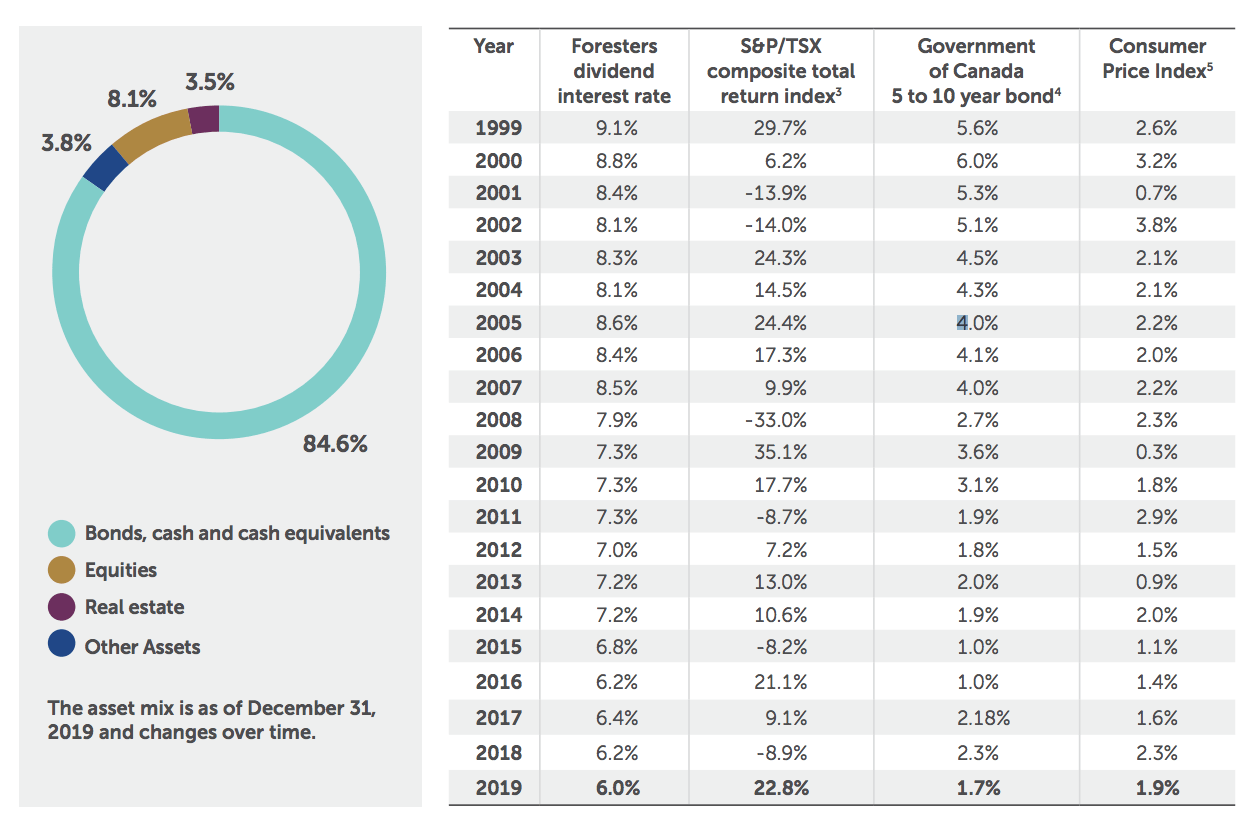

The next table is only relevant for participating policies. Participating policies pay a dividend, and it is a huge part of the performance of the cash value.

If you are using this data to choose a carrier, pair the table below with our 2026 comparison of the top 7 whole life insurance companies for cash value. The dividend history is the data source; the comparison explains how the carriers stack up for policy design, access to cash value, and long-term strength.

Get A High Dividend Paying Whole Life

We will get you the best dividend

What is participating policy?

A participating whole life insurance things know is one that pays dividends to the policyholder. The most competitive participating policies are from mutual companies.

The reason mutual companies pay dividends is that they do not have stockholders. So the only dividend they pay is to policyholders.

Why is the history of whole life dividends important?

We can take the highest dividend companies from today and pick the best one. However, we prefer to use today's rates and historical rates because it will give us a better idea of how the dividend will perform in the future.

Even though past performance doesn't indicate future performance.

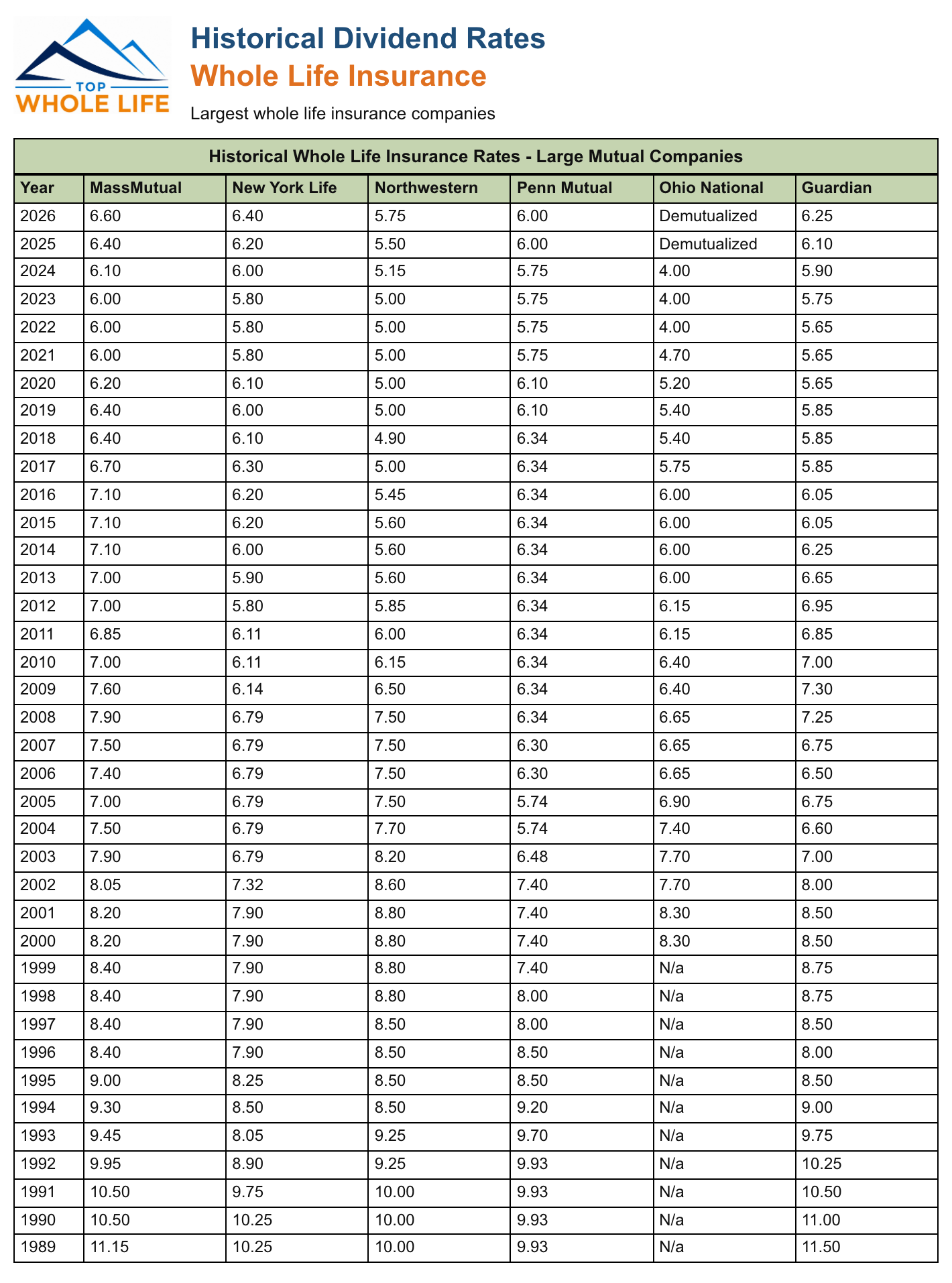

We took the following Historical Whole Life Dividends (webfiles2.nfp.com) that has incredible data, and updated the numbers:

We will keep updating it, and feel free to contact us, so we add a company.

| Company | 2026 | 2025 | 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Ameritas | TBD | 5.0 | 4.60 | 4.60 | 4.75 | 5.0 | 5.0 | 5.0 | 5.0 | 5.15 | 5.25 | 5.25 |

| Guardian | 6.25 | 6.10 | 5.9 | 5.75 | 5.65 | 5.65 | 5.65 | 5.85 | 5.85 | 5.85 | 6.05 | 6.05 |

| John Hancock | NA | NA | 4.25 | 4.25 | 4.25 | 4.75 | 5.0 | 5.0 | 5.15 | 5.15 | 5.3 | 5.55 |

| MassMutual | 6.60 | 6.40 | 6.1 | 6.0 | 6.0 | 6.0 | 6.2 | 6.4 | 6.4 | 6.7 | 7.1 | 7.1 |

| MetLife | NA | NA | NA | NA | NA | 4.7 | 4.7 | 4.7 | 4.7 | 5 | 5.1 | 5.1 |

| New England Financial (Brighthouse Financial) | NA | NA | NA | NA | 4.65 | 4.65 | 4.65 | 4.65 | 5 | 5 | 5 | 5 |

| New York Life | 6.40 | 6.20 | 6.0 | 5.8 | 5.8 | 5.80 | 6.1 | 6.0 | 6.1 | 6.3 | 6.2 | 6.2 |

| Northwestern Mutual | 5.75 | 5.50 | 5.15 | 5.0 | 5.0 | 5.0 | 5.0 | 5.0 | 4.9 | 5 | 5.45 | 5.6 |

| Penn Mutual | 6.00 | 6.00 | 5.75 | 5.75 | 5.75 | 5.75 | 6.1 | 6.1 | 6.34 | 6.34 | 6.34 | 6.34 |

| Ohio National | Demutualized | Demutualized | 4.0 | 4.0 | 4.7 | 5.2 | 5.4 | 5.4 | 5.75 | 6 | 6 | 6 |

| Foresters | NA | NA | NA | NA | NA | 5.8 | 6.23 | 6.23 | 6.58 | 6.83 | 6.65 | 6.42 |

Whole Life Insurance Dividend Rates for 2026

Major mutual carriers have announced 2026 dividend interest rates (DIR). Across the peers that have reported so far, rates are up 15 to 25 basis points versus 2025 — a continued lift as carriers adjust to the rate environment while money-market yields ease from their peaks.

| MassMutual | 6.60 |

| New York Life | 6.40 |

| Guardian | 6.25 |

| Penn Mutual | 6.00 |

| Northwestern Mutual | 5.75 |

| Foresters | NA |

Carrier dividend rate history (2026)

Jump to carrier-specific context and reviews:

- Mass Mutual dividend rate history — 6.60% DIR (2026)

- New York Life dividend rate history — 6.40% DIR (2026)

- Guardian dividend rate history — 6.25% DIR (2026)

- Penn Mutual dividend rate history — 6.00% DIR (2026)

- Northwestern Mutual dividend rate history — 5.75% DIR (2026)

Estimate how dividends affect cash value

Dividend rates alone do not show projected cash value — policy design, age, and funding level matter. For a personalized illustration with current 2026 rates, use our single whole life quote tool or compare carriers in the top 7 whole life insurance companies for cash value guide.

Whole Life Insurance Dividend Rates for 2025

2025 announcements for whole life dividend rates across the insurance industry have been released. To keep up with high yield savings account rates and the high Fed interest rate, the industry has had to increase dividends to continue to be attractive. The result is that dividend rates across the major whole life insurance firms are up between 20 basis points and 35 basis points. This increase in dividend yield while savings account rates are dropping should result in a positive year for Whole Life insurance, in general.

| MassMutual | 6.40 |

| New York Life | 6.20 |

| Penn Mutual | 6.00 |

| Guardian | 6.10 |

| Northwestern Mutual | 5.50 |

| Foresters | NA |

Whole Life Insurance Dividend Rates for 2024

2024 rates versus high yields savings accounts in early 2024 were just not attractive. Interest in whole life insurance for yield was challenged by risk free 5%+ money markets making whole life dividends look less attractive (Of course that is short term thinking on the part of the consumer).

| MassMutual | 6.10 |

| New York Life | 6.00 |

| Penn Mutual | 5.75 |

| Guardian | 5.90 |

| Northwestern Mutual | 5.15 |

| Foresters | NA |

Whole Life Insurance Dividend Rates for 2023

We are starting to get results on the 2023 announcements for dividends. All the dividends from the large mutual companies seem to have remained steady. As they come in we will update the list.

| MassMutual | 6.0 |

| New York Life | 5.8 |

| Penn Mutual | 5.75 |

| Guardian | 5.75 |

| Northwestern Mutual | 5.0 |

| Foresters | NA |

Whole Life Insurance Dividend Rates for 2022

Following are the dividend for participating policies in 2022.

| MassMutual | 6.0 |

| Foresters | 5.8 |

| New York Life | 5.8 |

| Penn Mutual | 5.75 |

| Guardian | 5.65 |

| Northwestern Mutual | 5.0 |

Whole Life Insurance Dividend Rates for 2021

We are starting to get results on the 2021 announcements for dividends. As they come in we will update the list.

| MassMutual | 6.0 |

| Foresters* | 5.8 |

| New York Life | 5.8 |

| Penn Mutual | 5.75 |

| Guardian | 5.65 |

| Northwestern Mutual | 5.0 |

| Ohio National | 4.7 |

*Foresters always announced dividend for the previous year. So their schedule is behind all other companies.

Whole Life Insurance Dividend Rates for 2020

At the end of the year, most companies start announcing their dividend rates for next year. Here are the whole life dividend rates for 2020 ahead of time. As we become aware of more, we will list them out.

| MassMutual | 6.2 |

| Penn Mutual | 6.1 |

| New York Life | 6.1 |

| Foresters* | 5.8 |

| Guardian | 5.65 |

| Ohio National | 5.2 |

| Northwestern Mutual | 5.0 |

*Foresters always announced dividend for the previous year. So their schedule is behind all other companies.

Whole Life Insurance Dividend Rates for 2019

Here is the full 2019 whole life dividend list from the largest and most important carriers.

| MassMutual | 6.4 |

| Foresters | 6.23 |

| Penn Mutual | 6.1 |

| New York Life | 6.0 |

| Guardian | 5.85 |

| Ohio National | 5.4 |

| Northwestern Mutual | 5.0 |

Whole Life Insurance Dividend Rankings for 2018

Here is a quick summary of the dividend rate from some of the largest/best companies that offer whole life insurance.

| Foresters | 6.58 |

| MassMutual | 6.4 |

| Penn Mutual | 6.34 |

| New York Life | 6.2 |

| Guardian | 5.85 |

| Ohio National | 5.4 |

| Northwestern Mutual | 4.9 |

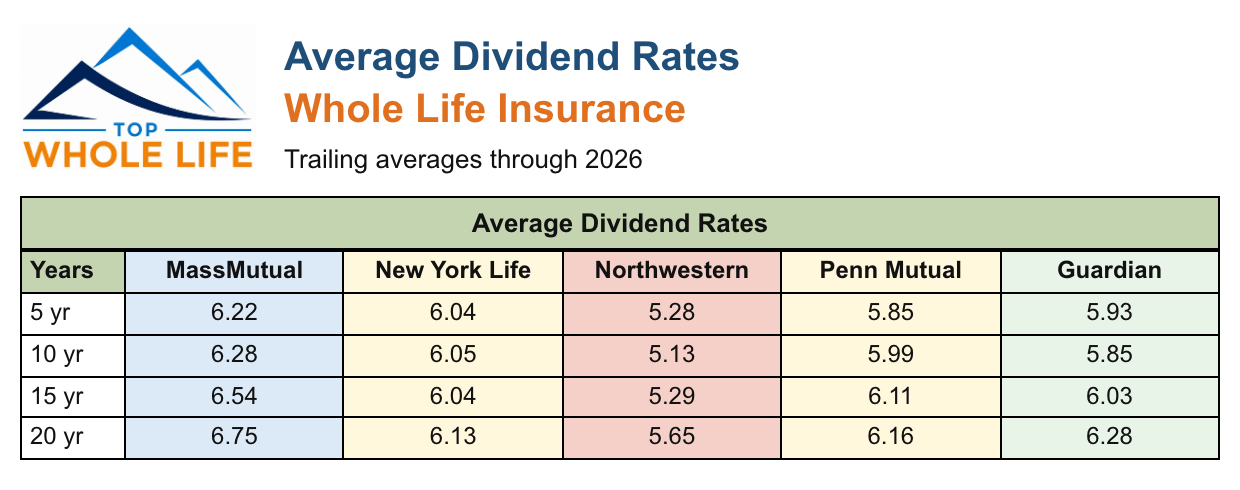

Whole Life Insurance Dividend Rates Historical Averages

It can be hard to understand all the data, so we created a simpler way for you to look at the information. The chart below shows trailing 5-, 10-, 15-, and 20-year averages through 2026 for the major mutual carriers we track.

| Company Name | 5 yr avg (2026) | 10 yr avg (2026) | 15 yr avg (2026) | 20 yr avg (2026) |

|---|---|---|---|---|

| MassMutual | 6.22 | 6.28 | 6.54 | 6.75 |

| New York Life | 6.04 | 6.05 | 6.04 | 6.13 |

| Guardian | 5.93 | 5.85 | 6.03 | 6.28 |

| Penn Mutual | 5.85 | 5.99 | 6.11 | 6.16 |

| Northwestern Mutual | 5.28 | 5.13 | 5.29 | 5.65 |

Which insurance company pays the best dividend?

For 2026 published dividend interest rates (DIR) among major mutuals on this page, MassMutual leads at 6.60%, followed by New York Life (6.40%), Guardian (6.25%), Penn Mutual (6.00%), and Northwestern Mutual (5.75%). Foresters has not announced a 2026 rate at the time of this update.

“Best” also depends on policy design, direct vs. non-direct recognition, and how you access cash value — not the headline rate alone. See our top 7 whole life insurance companies for cash value comparison for the full ranking methodology.

Mass Mutual dividend rate history

MassMutual's 2026 DIR of 6.60% is the highest published rate among the carriers tracked here. MassMutual carrier hub · MassMutual whole life review

New York Life dividend rate history

New York Life announced 6.40% for 2026 (+20 bps vs. 2025). New York Life carrier hub · NY Life whole life review

Guardian dividend rate history

Guardian's 2026 DIR is 6.25%. Guardian carrier hub · Guardian whole life review

Penn Mutual dividend rate history

Penn Mutual held 6.00% for 2026 (unchanged from 2025). Penn Mutual carrier hub · Penn Mutual whole life review

Northwestern Mutual dividend rate history

Northwestern Mutual's 2026 DIR is 5.75%. Northwestern Mutual carrier hub · NWM whole life review

Final Opinion

We used the previous tables, and in addition, we used the dividend analysis found at InsuranceProBlog to add more validation to our results (2016 Whole Life Insurance Dividend Analysis (theinsuranceproblog.com)).

Our rating for current whole life dividend strength:

#1 massmutual whole life insurance review

MassMutual has increased their dividend rate for 2026 to 6.6% — the highest published DIR among major mutuals. Also, we ran a historical analysis and found:

- MassMutual 15 year average dividend rate of 6.54% which also ranks at #1

- MassMutual 10 year average dividend rate of 6.28% which also ranks at #1

That is why it is our best pick for the top whole life insurance dividend.

#2 new york life whole life insurance review

New York Life is one of the best mutual companies out there. They have a fantastic track record and their dividend is stellar. In addition, their ratings are second to none. With a 2026 dividend rate of 6.4% — up 20 basis points from 2025 — New York Life ranks #2 among announced 2026 rates.

- New York Life Whole Life 15 year average dividend rate of 6.04%

- New York Life Whole Life 10 year average dividend rate of 6.05%

#3 guardian whole life insurance review

Guardian announced a 2026 DIR of 6.25% — up 15 basis points from 2025 — which ranks #3 among published 2026 rates on this page. Guardian has a long track record of competitive participating whole life dividends.

- Guardian 15 year average dividend rate of 6.03%

- Guardian 10 year average dividend rate of 5.85%

#4 penn mutual whole life insurance review

Penn Mutual held its dividend interest rate at 6.00% for 2026 (unchanged from 2025), which ranks #4 on published 2026 DIR but remains one of the most stable long-term performers. Penn has always had a very consistent dividend, even in a decreasing interest rate environment. They use direct recognition on their whole life contracts and their policies when illustrated are very attractive for long term cash value growth.

- Penn Mutual 15 year average dividend rate of 6.11% which ranks #2 on 15-year trailing average

- Penn Mutual 10 year average dividend rate of 5.99%

Do you have a dividend-paying whole life that you would like us to add?

The dividend rate is not everything. However, it helps grow top 7 whole life insurance companies for cash value.

To learn a little bit more about whole life insurance you should read:

whole life insurance for dummies

do you really want that overfunded cash value life insurance policy

whole life insurance faqs much whole life insurance cost

comparing insurers the mutual and stock insurance company