Participating Whole Life Insurance | Top Whole Life

Updated Dec 14th 2019

Participating Whole Life Insurance

As you shop for life insurance, there's sure to be one thing on your mind: the financial security of your family in the event that you pass on.

With the help of whole life insurance, you can guarantee that your loved ones will receive a death benefit upon your death. This isn't fun to think about, but it definitely gives you peace of mind.

Why Whole Life?

A whole life insurance policy provides permanent insurance, ensuring that your family can cover needs such as:

- Funeral and final expenses

- Income for your surviving spouse and children

- Daily living expenses

While all of this is important, there is something else you need to know about whole life insurance: it can be one of the best "investments" you ever make.

In addition to financial support for your family after your death, many whole life insurance policies offer the benefit of cash value accumulation.

In short, the cash value of a policy is the amount that a company will pay to a policyholder in the event that coverage is terminated.

As long as your policy remains active, due to you paying your premium in full and on time, it will continue to accumulate value on an annual basis.

With this type of policy, you're getting more than a death benefit. You're also accumulating cash that can be used during your lifetime, or by your family after you are gone.

The Right Whole Life

But make sure you look for the right kind of whole life insurance.

One of the most important aspects to consider is getting a: Participating Whole Life Insurance

Participating means that you participate in the performance of the company. The better the company you bought does, then the more they will share with you. You will receive a dividend that helps the policy grow.

Not only it helps grow the cash value, but also the death benefit.

Most participating whole life policies get dividends every year.

Who Should Consider A Participating Whole Life?

Whole life insurance can be great, but it definitely not for everyone. If you need a large amount of coverage, and the budget is tight, you should not get a whole life.

You should be looking to get single whole life quote.

However, if you have extra income. Or if you are a good saver, you can definitely consider a participating policy.

That doesn't mean you should get a term policy thought. You should always have the right amount of coverage.

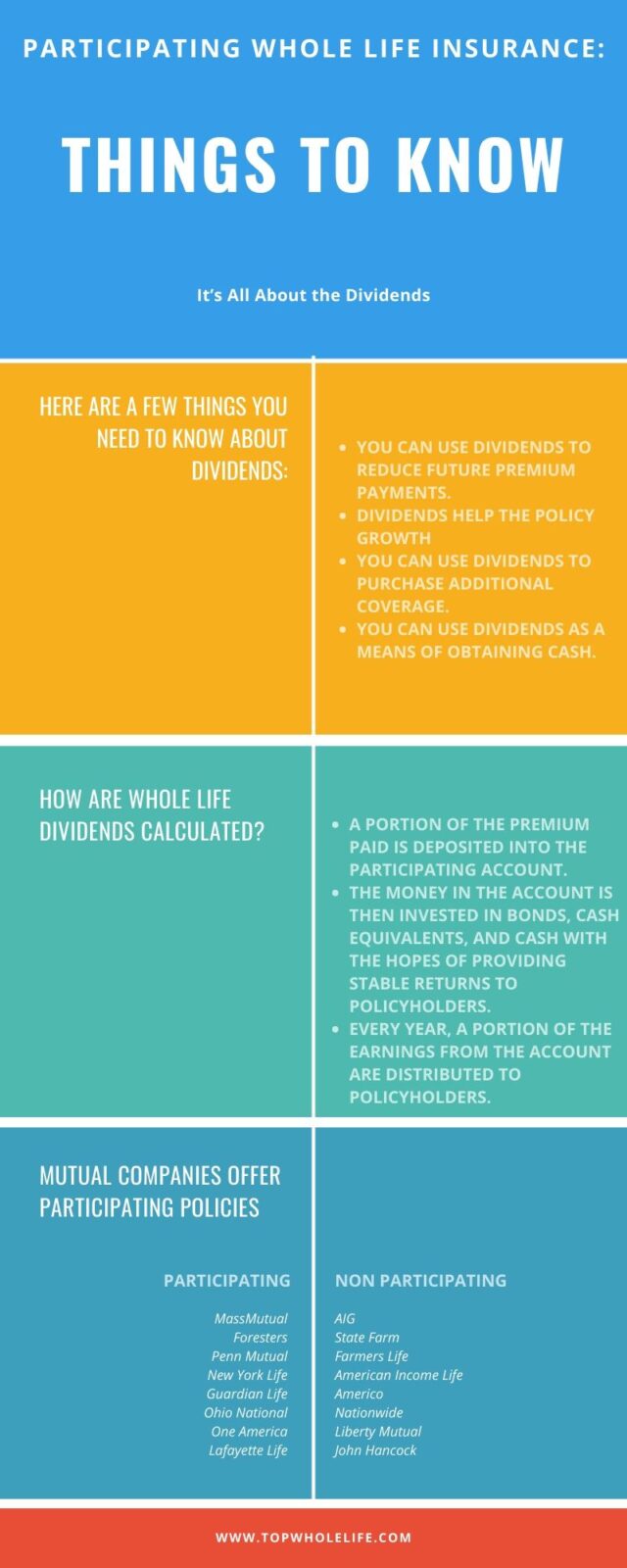

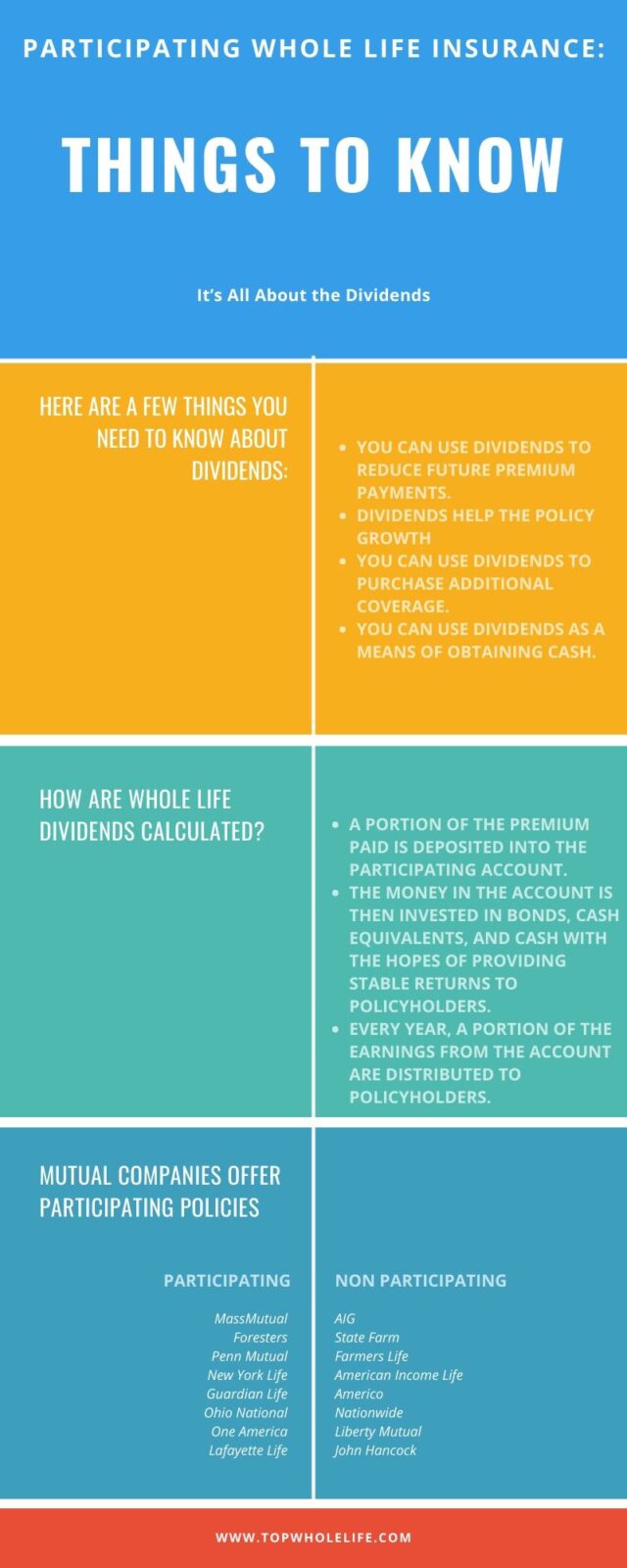

It's All About the Dividends

As we mentioned, a participating whole life insurance policy is eligible to earn dividends. Generally speaking, a dividend is nothing more than earnings that a company distributes to policyholders.

Not all companies offer participating whole life insurance policies. Many years ago, every insurance company had a participating policy, but that trend has changed. Most insurance companies focus on term insurance, which is great for providing you with a large death benefit for an affordable price.

Here are a few things you need to know about dividends:

- You can use dividends to reduce future premium payments.

- whole life insurance investment

- You can use dividends to purchase additional coverage.

- You can use dividends as a means of obtaining cash.

However, remember this: although dividends are expected, they are never guaranteed.

When you purchase a policy from a whole life participating company, you do so with the idea that you will receive dividends in the future. Many of the large mutual companies have paid dividends for hundreds of years.

The following list is a few of the large mutual companies that offer participating policies, and that have paid dividends for over 100 years:

- MassMutual

- Penn Mutual

- Guardian

- New York Life

- Northwestern Mutual

Related: whole life insurance dividend rate history

How Are Whole Life Dividends Calculated?

In reality, dividends are calculated based on many factors. Consider the following:

- A portion of the premium paid is deposited into the participating account.

- The money in the account is then invested in bonds, cash equivalents, and cash with the hopes of providing stable returns to policyholders.

- Every year, a portion of the earnings from the account are distributed to policyholders.

Dividend payouts can change significantly from one participating whole life insurance company to the next. The reason dividends vary is largely based on the financial stability and growth of the company offering the whole life.

Some companies offer whole life dividends as high as 6.2%.

What Makes A Dividend?

There are many factors that impact dividend payouts. Here is a list of a few:

- The mortality rate of policyholders

- The fund's performance

- Expenses

- Interest Rates

- Financial Projections

- Competitive Advantages

That is just a few of the factors.

The General Account

To begin with, if you really want to understand the dividend you have to look under the hood of a life insurance company.

Life insurance companies get premiums from all of the policyholders. Then, all of these premiums get invested into something called a "General Account".

Because this general account is invested with a very very long term view, it has to limit risk. That's why most of the investments in the account are bonds, high-quality stocks, and real estate.

The performance of this general account is what allows companies to pay more or less in dividends.

Non Participating vs. Participating Example

So now let's look at an actual example with numbers. The following is a whole life for a 35 year old male with excellent health. We will compare numbers with and without dividends so you see the difference long term.

| Non Participating (No Dividend) | ||||

| Age | 50 | 65 | 75 | 85 |

| Cumulative Premium | $44,925 | $89,850 | $119,800 | $149,750 |

| Total Cash Value | $42,070 | $104,635 | $150,800 | $192,713 |

| Total Death Benefit | $250,000 | $250,000 | $250,000 | $250,000 |

So let's compare the previous numbers to a whole life participating policy. Remember that the dividends are what helps the policy grow.

| Participating (With Dividend) | ||||

| Age | 50 | 65 | 75 | 85 |

| Cumulative Premium | $44,925 | $89,850 | $119,800 | $149,750 |

| Total Cash Value | $50,502 | $174,357 | $328,757 | $565,569 |

| Total Death Benefit | $274,108 | $377,834 | $507,991 | $704,232 |

If you look at the numbers on this example, this client at age 65 would have $70,000 more in the participating policy.

Mutual Companies Offer Participating Policies

One of the easiest ways to find out if a company offers participation policies is to see if they are a "mutual" insurer. While most companies that have the word "mutual" in their name, have participating policies, it is not always the case.

As you can see, there are certain companies that used to be or still are mutually owned but don't have participating policies:

- Liberty Mutual

- John Hancock

- Mutual of Omaha

Here is a table that will show participating vs non-participating whole life companies:

| Participating | Non Participating |

| MassMutual | AIG |

| Foresters | State Farm |

| Penn Mutual | Farmers Life |

| New York Life | American Income Life |

| Guardian Life | Americo |

| Ohio National | Nationwide |

| One America | Liberty Mutual |

| Lafayette Life | John Hancock |

In general, we would always recommend sticking to Participating whole life policies.

At the end of the day, the dividend makes all the difference.

Final Thoughts

If you're going to purchase whole life insurance, you might as well do so with the idea that this can double as an investment.

Finally, there are many participating whole life insurance companies, with some of the best including:

- massmutual whole life insurance review

- penn mutual whole life insurance review

- new york life whole life insurance review

- northwestern mutual whole life insurance review

While there is no way of knowing what the future holds, a participating whole life insurance policy could pay annual dividends for the rest of your life.single whole life quote