The Complete and Unbiased Review of Banner Life Insurance

Ten Americans Life Insurance Protect Ability Live (businesswire.com) believe that life insurance provides long-term financial protection. Only half of these individuals, however, actually own some form of life insurance.

The numbers were higher in 2018, wherein about Facts Statistics Life Insurance (Insurance Information Institute) had life insurance. Still, 20% of those who did have one said that it wasn't enough.

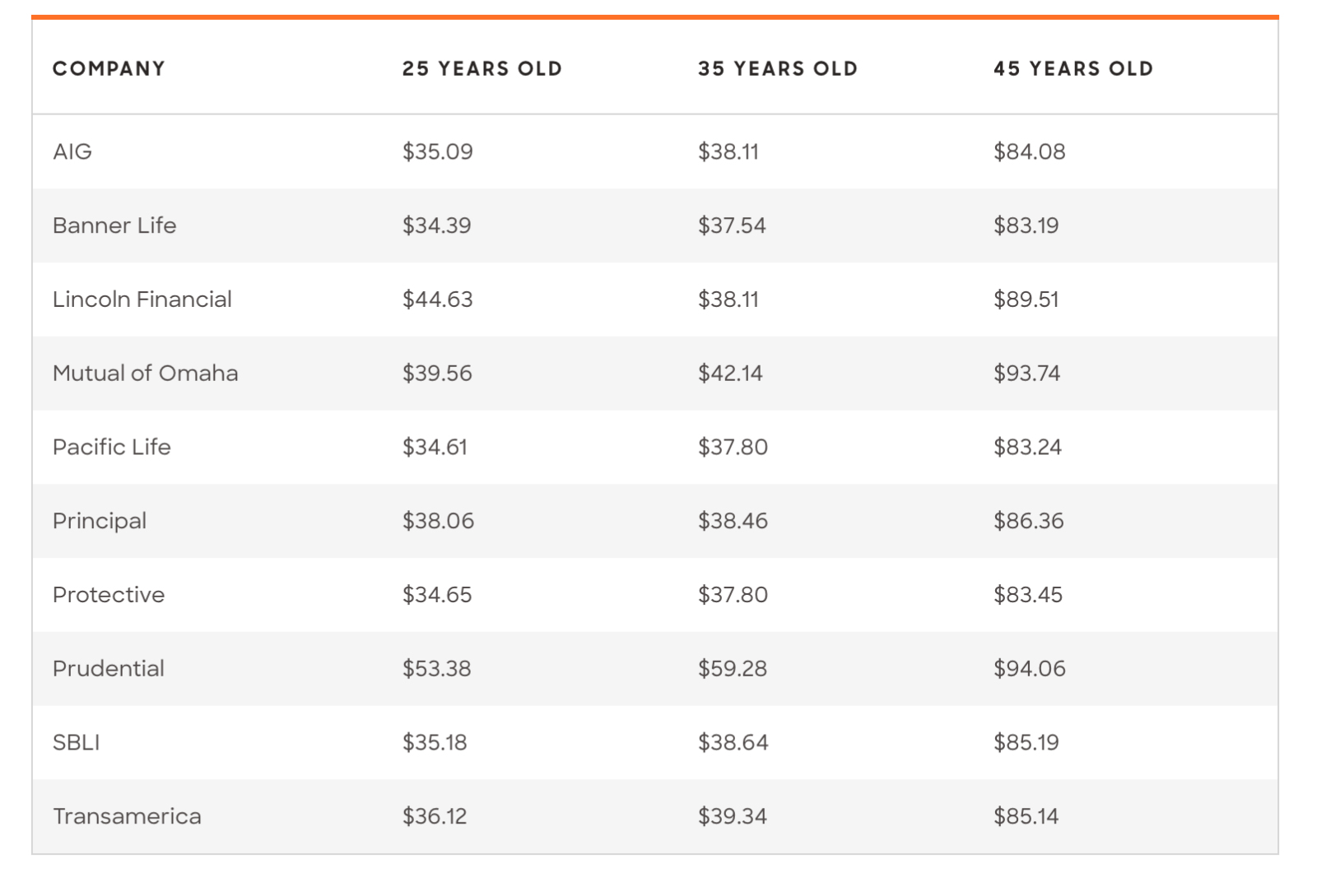

That said, if you've been considering buying a policy, now is the best time to compare your options. The sooner you do, the sooner you can get your life insured. This then translates to more competitive rates and premiums.

As for life insurance coverage options, Banner Life Insurance is one of the most popular in the US. At the moment, the company serves about Claims Infographic (lgamerica.com).

The big question now is, what exactly are these Banner Life offers and what makes them a good deal? What types of life insurance products do they offer and how much can you expect to pay?

This Banner Life Insurance review will answer all these and more, so be sure to keep reading!

A Quick History of Banner Life

Banner Life is one of the two underwriters and issuers of Legal and General life insurance. The other one is William Penn Life Insurance Company of New York. Together, these two serve the entire US, plus the District of Columbia.

Banner Life, however, covers the 49 states (and D.C.), with the exception of the New York State. William Penn is the one that caters to the life insurance needs of the Empire State's residents.

Legal and General itself has a history that dates back to the mid-1830s, so it's been around for Legal Generals Retirement Opportunity (sharesmagazine.co.uk). The Banner Life Insurance company entered the picture in 1981. That said, it has been protecting policyholders in the US for almost four decades now.

Banner Life Insurance Review: Pros and Cons Overview

Before we delve into the nitty-gritty of Banner Life policies, let's go through the main pros and cons first.

The Good

A solid financial standing and low rates make Banner Life stand out from the rest. A Solid Company Rating

In 2019, the Banner Life Insurance company rating from COMDEX was an impressive 94. COMDEX is a composite score that averages ratings from major insurance rating organizations. There are four such organizations: A.M Best, Fitch, Moody's, and Standard and Poor's (S&P).

The higher a COMDEX rating is (from a scale of 1 to 100), the better a company's ranking. So, with a score of 94, Banner Life has scored 94% higher than other insurers.

This signals that Banner Life has a solid financial status. Meaning, you can trust the company to back you up when you do experience life difficulties. Better Premium Rates for Those With Health Conditions

Most insurance carriers raise their rates for people who have medical conditions. That includes the AboutChronicDisease (nationalhealthcouncil.org) who have a chronic disease. Heart disease, cancer, and diabetes are the top three most common long-term diseases in the US.

The good news is, Banner Life is a little less strict -- it doesn't hone in on a single risk factor. Instead, it looks at a person's general health. So, if you have a single health issue but you are in general good health, Banner is more likely to give you better rates. Extensive Term Length Options

Whether you want a term life insurance for 10 years, 15 years, or 40 years, Banner Life has you covered. Many other insurance companies offer only up to 30 years.

The Not-So-Good

There's no perfect life insurance company, and Banner still has quite a ways to reach "perfection".Offers Only Three Types of Life Insurance Products

These include term life, universal life, and final expense insurance. Single Payment Option for Monthly Payments

If you want to pay premiums on a monthly basis, you can only do so with an automatic bank draft. Banner Life does, however, allow EFT, check, and PayPal for other payment frequencies. Limited Customer Service Hours

Banner's customer service only operates during Eastern time business hours. So, you'd have to wait for the next business day (or week) if you want to get in touch with them.

A Crash Course on Banner Term Life Insurance

Term life insurance is the most affordable type of life insurance coverage you can get. That's because it has an "expiration" date, hence the term "term". For instance, if you take out a 10-year term policy, you'll receive coverage for the next 10 years.

That's if you pay premiums on time. Otherwise, your policy will lapse, and it'll no longer provide you coverage.

You Can Covert Your Banner Term Life Policy

What if your finances stabilize and you want to get a permanent life insurance policy? Banner Life allows you to do exactly that -- you can convert your term policy into universal life! You can request your policy conversion anytime or until you turn 70.

You May Be Eligible for a Waiver of Premium

Banner Life also gives a waiver of premium, in case you sustain a long-term injury or illness. Keep in mind that brain injuries alone cause long-term disability in Tbi Report To Congress (CDC) Americans each year. What's more, Facts (Social Security Administration) in their 20s become disabled in the US every year!

Banner Life's waiver of premium will keep protecting you in case of total disability. You only have to provide proof of the disability that lasts for at least half a year. Banner Life will then waive your premiums throughout this period of incapacitation.

What About the Costs?

According to Banner, its term life insurance products start with rates for as low as $7 a month. Keep in mind, however, that the $7/month quote may only be the initial price. You can request term life insurance without personal information about yourself to get a gauge of how much you'd pay.

As for premiums, this will depend on how much you'd want your death benefit to be. With Banner Life, the minimum death benefit is $100,000, with the max being $10 million.

How About Coverage Terms?

As for terms, the minimum is 10 years, with increasing terms of five-year increments. Meaning, you can get a term policy for 15, 20, 25, 30, 35, or 40 years.

The Permanent Life Insurance Offers From Banner Life

Universal life insurance, like whole life insurance for beginners, is a permanent life insurance policy. The whole life vs universal life insurance is that with whole life, your premiums will never change. Whereas universal life is flexible -- you can adjust your premiums every year.

As a permanent life insurance policy, universal life remains in place for as long as you want to. Of course, you'd need to stay up-to-date with your payments, so that your coverage won't lapse. If your needs change, such as if you're getting married or having a child, you can adjust your benefits.

Guaranteed Death Benefit

Universal life is also similar to whole life in that it also has a guaranteed death benefit whole life. However, since you can "revise" your universal life plan, you can increase your benefits. Banner Life also allows you to pay a level premium for guaranteed coverage.

Aside from the guaranteed death benefit, you also have guaranteed cash value.

The Short Pay Guarantee Benefit

Banner Life's Short Pay Guarantee allows you to customize your premium payments. This way, you can be 100% sure that you can pay for your policy up until its maturity. By the way, Banner Life's maturity runs until its policyholders' 120th birthday.

Since you'll go into retirement way before you turn 120, you can "shorten" your payment term. With the Short Pay Guarantee, you can consolidate all your premium payments into, say, 15 years. So, you'll only pay premiums for 15 years but still get coverage for life.

This benefit can be helpful if life insurance in your 40s your ultimate guide and you want to ensure coverage before you enter retirement.

What About Banner Life's Final Expense Policy?

Final expense life insurance also goes by the name "guaranteed whole life insurance". The "guaranteed" there refers to how such policies provide guaranteed acceptance.

Banner Life's final expense policies guarantee acceptance for people aged 50 to 80. You don't have to worry about getting rejected due to the condition of your health. Moreover, there's no medical exam required to purchase this policy.

You won't even have to answer a lengthy questionnaire about your health!

No Changes to Premiums

In addition, your premiums will never increase -- you'll pay for the same amount that you did the first time. Even if there's a not-so-good change to your health status, you'll pay the same amount.

Speaking of which, you'll only pay for premiums up until your 95th birthday. After that, you'll continue to receive coverage without further payments.

Build Cash Value Over Time

As a type of permanent life insurance, Banner Life's final expense also builds cash value. That means you also get to enjoy an extra source of funds! After some time, you can already borrow against it.

Explore and Compare Insurance Offers From Banner Life Now

There you have it, a comprehensive look on Banner Life Insurance policies. Now that you know more about the company's offers, you can better decide if they're a good fit for your needs. As with all insurance products though, it's best to take the time to explore and compare your options.

That's where we come in to help -- for starters, use our guide on how to how to shop for life insurance during the pandemic right at the safety of your home. You can also send a direct get a whole life quote and we'll even do the legwork of comparing them for you!