Ohio National Whole Life Insurance Review | Good or Bad [Update 2025]

![Ohio National Whole Life Insurance Review | Good or Bad [Update 2025]](/images/wp-content/uploads/2017/06/1.png)

Updated October 17, 2018

In this article you will find our Ohio National Whole Life Insurance Review.

However, let's start by looking at the company first. Ohio National, also known as the Ohio National Life Insurance Company, is one of the more reputable mutual insurance companies in the United States.

In 1909, Ohio National was founded as a stock company. However, 50 years later, it made the switch to a mutual company. Then, in 1998, it reorganized as a mutual insurance holding company, with an official name of Ohio National Mutual Holdings, Inc.

The Good

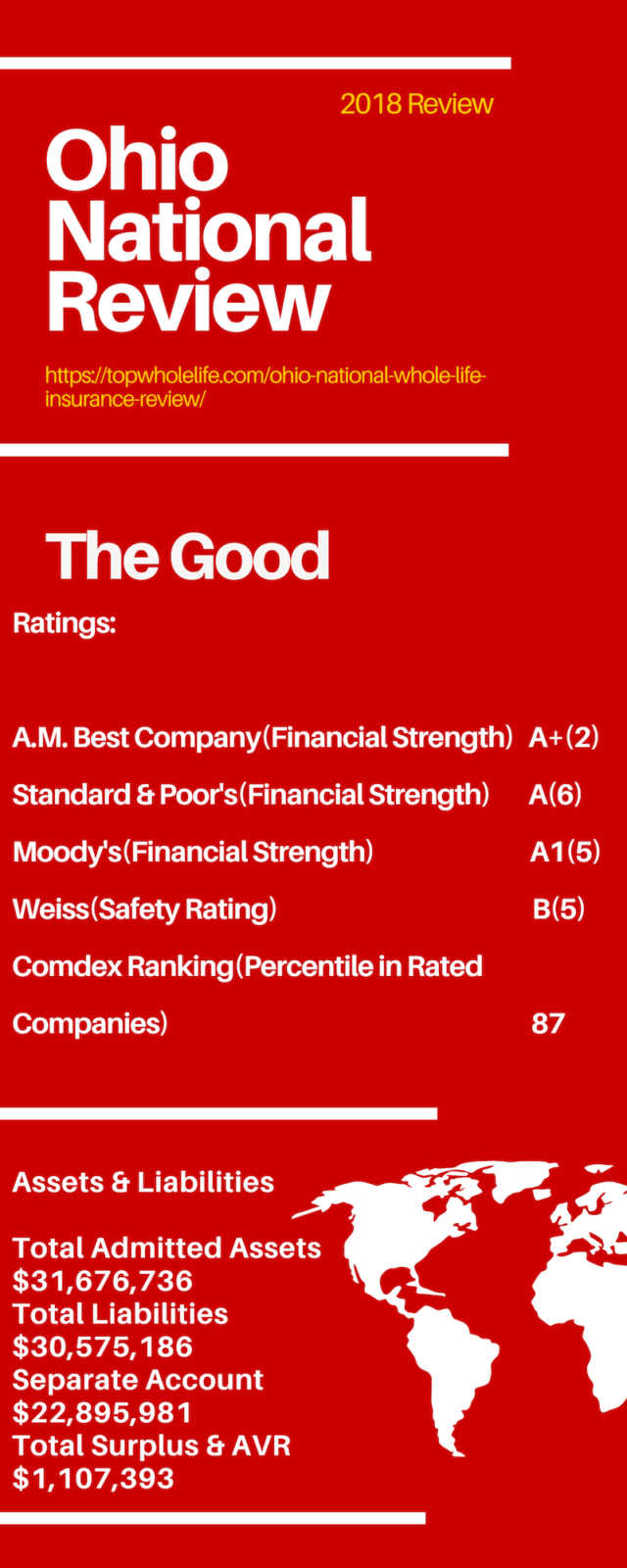

Good Rating

When shopping for whole life insurance, it's imperative to find a company with a good reputation. Furthermore, knowing that the company is on stable financial ground is a must.

This is why Ohio National is a consumer favorite. For more than 100 years, the company has been one of the highest rated in the industry.

Its current ratings include:

- Moody's: A1, which is the fifth highest rating.

- A.M. Best: A+ Superior, which is the second highest rating.

- Standard & Poor's: A, which is the sixth highest rating.

As you can see, Ohio National has some room for improvement, but there aren't many companies that score this high across the board in regards to its ratings.

Selection

In reality, it can be difficult to purchase whole life insurance for a variety of reasons, including the fact that there are many companies selling many products.

However, with Ohio National, you gain access to a large selection of products, all of which have something special to offer a particular type of consumer.

Whole Life Cash Value Rich Products

- Prestige 10 Pay: this is a 10 year, limited pay, whole life insurance policy. After paying your premium for 10 years, you are no longer required to make additional payments.

- Prestige Max: this type of policy is paid until you reach age 65 or for 10 years after purchase, whichever is later, and is designed to help you maximize savings and dividends to grow your cash value.

- Prestige Max II: This is a high premium and high cash flow products. It grows cash value very rapidly. Great for deferred compensation and executive bonus plans. It's even better than Prestige Max.

Whole Life Products For Death Benefit and Low Price

- Prestige Value III: this is the lowest priced whole life insurance policy. Even with cheaper prices, you still have the opportunity to collect dividends.

- Prestige 100: premiums are paid until you reach age 100, with the policy providing guaranteed death benefit protection.

Available Health Classes

Here is the list of available health ratings that you can get in an Ohio National whole life policy. We list them from best to worst:

- Super Preferred

- Preferred Nonsmoker

- Select Nonsmoker

- Nonsmoker

- Select Smoker

- Smoker

The better health rating that you get, the lower the price you will pay.

Participating Whole Life Insurance

Many people have come to find that whole life insurance is good for more than a guaranteed death benefit.

When you purchase a policy through a participating whole life company, such as Ohio National, you can also earn dividends as a way of accumulating cash.

Here is something special that the company shares on its website:

"For more than 90 consecutive years, Ohio National has paid dividends to our policyholders and, although dividends are not guaranteed, we expect this practice to continue."

How many other companies can claim that?

The Not So Good

Customer Service

Ohio National does almost everything right, however, there's one area in which the company needs to improve, customer service

For example, it's not always as simple as it should be to find a local agent who can provide a quote and walk you through the buying process.

Furthermore, if you require assistance as a policyholder, you'll need to contact the company via phone for guidance.

Ohio National also has a reputation for not wanting to work with internet leads. Your lead request will ultimately be sent to an agent to call you and talk over the phone.

If you request a quote online, you will be provided with a quote that is designed to bet all the others online. This rate will look great from a pricing perspective but will not accurately project your final heath class after underwriting is completed.

Finances

Ohio National shares a variety of financial information on its website, including the following numbers for 2017:

- Total GAAP revenue (excluding realized gains and losses) increased 10.4 percent to $2.2 billion.

- GAAP equity grew at record levels. Equity (excluding mark-to-market) grew to $2.3 billion, an increase of 0.1 percent. Equity (including mark-to-market) grew to $2.6 billion, a 2.3 percent increase.

- Core earnings increased 2.7 percent to $181.5 million. The increase relates to higher than planned fee-related income, offset by higher than planned claims and mortality and less than planned investment income and margins.

- For the 94th consecutive year, Ohio National paid dividends to participating whole life policyholders. A total of $92.0 million was paid or credited to participating policyholders.

Dividend Rate

As noted above, Ohio National has paid out a dividend for more than 80 consecutive years. Here is a look at its recent dividend history and compare it to other whole life insurance dividends:

| Year

|

Ohio National

|

Guardian

|

MassMutual

|

New York Life

|

Northwestern Mutual

|

Penn Mutual

| | --- | --- | --- | --- | --- | --- | --- | | 2019 | 5.4 | 5.85 | 6.4 | 6.0 | 5.0 | 6.1 | | 2018 | 5.4 | 5.85 | 6.4 | 6.1 | 4.9 | 6.34 | | 2017 | 5.75 | 5.85 | 6.7 | 6.3 | 5 | 6.34 | | 2016 | 6 | 6.05 | 7.1 | 6.2 | 5.45 | 6.34 | | 2015 | 6 | 6.05 | 7.1 | 6.2 | 5.6 | 6.34 | | 2014 | 6 | 6.25 | 7.1 | 6 | 5.6 | 6.34 | | 2013 | 6 | 6.65 | 7 | 5.9 | 5.6 | 6.34 | | 2012 | 6.15 | 6.95 | 7 | 5.8 | 5.85 | 6.34 | | 2011 | 6.15 | 6.85 | 6.85 | 6.11 | 6 | 6.34 | | 2010 | 6.4 | 7 | 7 | 6.11 | 6.15 | 6.34 | | 2009 | 6.4 | 7.3 | 7.6 | 6.14 | 6.5 | 6.34 | | 2008 | 6.65 | 7.25 | 7.9 | 6.79 | 7.5 | 6.34 | | 2007 | 6.65 | 6.75 | 7.5 | 6.79 | 7.5 | 6.3 | | 2006 | 6.65 | 6.5 | 7.4 | 6.79 | 7.5 | 6.3 | | 2005 | 6.9 | 6.75 | 7 | 6.79 | 7.5 | 5.74 | | 2004 | 7.4 | 6.6 | 7.5 | 6.79 | 7.7 | 5.74 | | 2003 | 7.7 | 7 | 7.9 | 6.79 | 8.2 | 6.48 | | 2002 | 7.7 | 8 | 8.05 | 7.32 | 8.6 | 7.4 | | 2001 | 8.3 | 8.5 | 8.2 | 7.9 | 8.8 | 7.4 | | 2000 | 8.3 | 8.5 | 8.2 | 7.9 | 8.8 | 7.4 | | 1999 | N/A | 8.75 | 8.4 | 7.9 | 8.8 | 7.4 | | 1998 | N/A | 8.75 | 8.4 | 7.9 | 8.8 | 8 | | 1997 | N/A | 8.5 | 8.4 | 7.9 | 8.5 | 8 | | 1996 | N/A | 8 | 8.4 | 7.9 | 8.5 | 8.5 | | 1995 | N/A | 8.5 | 9 | 8.25 | 8.5 | 8.5 | | 1994 | N/A | 9 | 9.3 | 8.5 | 8.5 | 9.2 | | 1993 | N/A | 9.75 | 9.45 | 8.05 | 9.25 | 9.7 | | 1992 | N/A | 10.25 | 9.95 | 8.9 | 9.25 | 9.93 | | 1991 | N/A | 10.5 | 10.5 | 9.75 | 10 | 9.93 | | 1990 | N/A | 11 | 10.5 | 10.25 | 10 | 9.93 | | 1989 | N/A | 11.5 | 11.15 | 10.25 | 10 | 9.93 | | | | | | | | |

Just announced! Check out: ohio national announces 2019 dividend

Final Word

The whole life insurance industry is crowded, but Ohio National has been a top player for many years.

In addition to its large selection of policies, the company is known for its strong dividend performance and dedication to its policyholders. If you are ok with choosing a smaller company, you will have a great performing whole life insurance.

Check out our some of our other reviews: liberty mutual whole life insurance review and guardian whole life insurance review.