American Income Life Insurance Reviews | Top Whole Life

American Income Life Whole Life Insurance Review

American Income Life Insurance Company sounds like a company that would provide high-quality whole life insurance coverage to a large audience.

While it has several products to choose from, these continually come up short compared to the competition.

If all you are looking for is a quote to compare, you can get one here:

Compare American Income Life vs. The Competition

Get A Whole Life & Cheap Prices

The Good

- Strong Financial Ratings

- Lot's of Riders

- Good Product List

- Solid Customer Base

\

The Bad

- Bait And Switch

- Non-Participating Whole Life

- Poor Customer Service

- Hard To Find Your Agent

Here are some crucial details and statistics associated with the company:

- American Income Life Insurance Company was founded in 1951 based in Waco, Texas.

- American Income Life Insurance is a wholly-owned subsidiary of Investors Globelifeinsurance (investors.globelifeinsurance.com) (NYSE: GL), an S&P 500 Company (About (ailife.com))

- The company is licensed in 49 states, the District of Columbia, and Canada.

- Along with their New York subsidiary National Income Life, American Income Life has combined assets of more than $4.2 billion with more than $59 billion of life insurance in force in 2017 (as of 3/18).

With numbers like these, it's only natural for some consumers to navigate toward American Income Life Insurance Company.

However, it's also important to compare all the finer details to other providers, as this is the only way to understand what's available fully. (data from About (ailife.com)).

The Good

Strong Financial Rankings

While some companies fall short in this area, American Income Life Insurance Company has remained relatively strong over the years.

Consider the following:

- AM Best: A+

- Fitch: A+

- S&P: AA-

You can confidently purchase a policy from the company, knowing that it's likely to be around in the future.

Solid Customer Base

There is no denying that American Income Life Insurance Company is smaller than some whole life insurance industry leaders.

Even so, the company has grown to more than two million policyholders throughout the United States and Canada.

When you consider its $59 billion of life insurance in force, you have a company with a solid customer base. One of their main focus is to:

"AIL's efforts are focused on creating more union jobs. We proudly proclaim our status as a 100% union label Company."

As you can see, they have a decent size customer base.

Wide Product List

American Income Life Insurance Company sells more than just whole life insurance. They have many different policies like:

- Hospital Indemnity

- Cancer Protection

- Critical Illness

- Whole Life Insurance

- Term Insurance

These products offer an excellent array for their customer base.

For example, its term life policies are very popular.

The Not So Good

Non-Participating Whole Life Insurance

When shopping for whole life insurance, it's best to avoid non-participating companies.

American Income Life's whole life has a 4.5% guaranteed rate, enough to attract many consumers. However, it's important to note that there is no dividend on top of this.

Here's why this is a big deal: many other companies offer both a guaranteed rate and a dividend. With this dividend, it's easier to see that your policy will grow much faster with each passing year. As a result, your cash value grows faster, and your death benefit can also grow.

As a comparison, please look at our historical dividend article: whole life insurance dividend rate history.

This one pitfall alone is reason enough to shy away from American Income Life Insurance Company's whole life policies instead of choosing a participating whole life insurance things know.

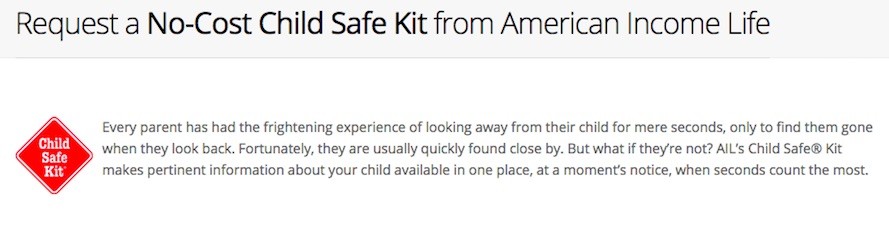

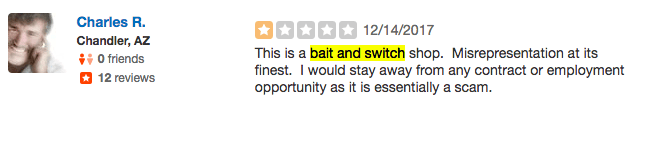

Bait And Switch

Unfortunately, there have been many instances of clients complaining about a bait and switch on the sale of Child Safety Kits. These kits seem like a fantastic idea:

In reality, everyone needs life insurance, but it's strange when you expect one thing and get something else.

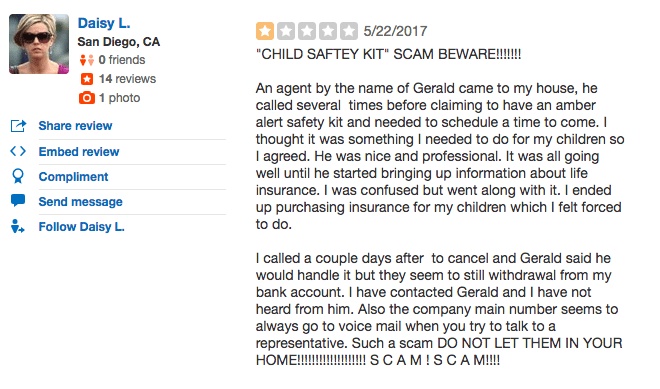

Now let's look at some other reviews that are worrying.

Check out some of the American Income Life Insurance Company San Diego (yelp.com):

Here are some other bad comments on the marketing tactic:

The kits can be a great idea if sold properly. But this strange way agents American Income Life Ail Review (davidduford.com) policies can leave customers feeling cheated, and that's why they call it a scam.

Bad Customer Service

There is nothing more important than keeping customers happy in today's day and age. But unfortunately, it only takes a few bad online reviews to harm a company.

Unfortunately, the American Income Life Insurance Company finds itself in this position. As a result, hundreds upon hundreds of online reviews, both from individual policyholders and employers, are unhappy with the company.

Some people complain that it takes entirely too long to purchase a policy. You may be disappointed with the customer service. Some customers say that they are unable to get in touch with a company representative when they have questions or concerns.\Don't take our word for it read more directly from the Better Business Bureau: Click Here to read more

It's good that American Income Life Insurance Company has strong financial ratings, but this doesn't do anything for the company regarding its online reviews.

Final Word

If there is one thing you should know about whole life insurance, it's this: many reputable companies are selling high-quality policies while providing the best possible customer service.

Our American Income Life Whole Life Insurance Review is not favorable.

American Income Life Insurance Company has been around for more than 65 years, but it's not the right choice for whole life insurance buyers for two reasons:

- It is a non-participating company, meaning your money will go further elsewhere.

- It doesn't have positive reviews from other consumers.

With so many choices, you should never settle when buying a whole life insurance policy. This is an important purchase that you need to get right the first time around. American Income Life Insurance Company doesn't allow you to purchase with peace of mind.

See How AIL Stack vs. The Competition

Get A Whole Life & Cheap Prices

Company Contact Information

American Income Life Insurance Company

Website: Ailife (ailife.com) Phone Number: (800) 433-3405 Address: 1200 Wooded Acres Dr. Waco, TX 76710