Sagicor Whole Life Insurance Review | You Haven't Considered Them?

Sagicor Whole Life Insurance Review

Some whole life insurance companies have a great reputation for providing high quality policies, affordable prices, and top of the line customer service.

Other companies fall short in all these areas, continually disappointing consumers who choose to do business with them.

And then there are those companies that fall somewhere in between. This is where you will find the Sagicor Life Insurance Company.

All in all, Sagicor is a solid company that is financially stable. However, its whole life insurance is overpriced. Along with this, it doesn't have a dividend, which immediately pushes it below the competition.

Also known as Sagicor Financial Corporation, here are some key points associated with the company:

- The company operates in Latin America and the Caribbean region.

- Its total assets as of September 2013 were $5.78 billion.

- It has several divisions for providing coverage to consumers in other parts of the world. These include: Sagicor Capital Life, Sagicor Panama, and Sagicor Group Jamaica.

These details show that Sagicor definitely has a strong following. However, as noted above, there are some things that continue to hold the company back from becoming a bigger player.

The Good

Strong Financial Strength

Some companies don't excel in this area, making it difficult for consumers to trust that they will be in business well into the future.

Sagicor doesn't fit into this group, with the company in solid (but not the best) financial standing at the present time. Consider these ratings:

- AM Best: A- (Excellent)

- Fitch: B

- S&P: B

As you can see, Sagicor trails some companies in regards to financial strength, but it remains on stable ground.

Variety

While some companies only offer one type of whole life insurance, Sagicor provides a variety of policies to choose from.

All of its Whole Life Series Plans have something unique to offer, with these providing fixed rate premiums and a guaranteed death benefit.

One of its most popular policies is the "Life Paid Up At 65" plan. With this, once you reach the age of 65, premiums are no longer required. And even though you're no longer paying for coverage, your policy remains in effect until you pass on.

Another, unique aspect Sagicor offers a Whole Life Insurance No Medical Exam (abramsinc.com), which is great if you do not want to go through the hassle of doing a medical exam.

The Not So Good

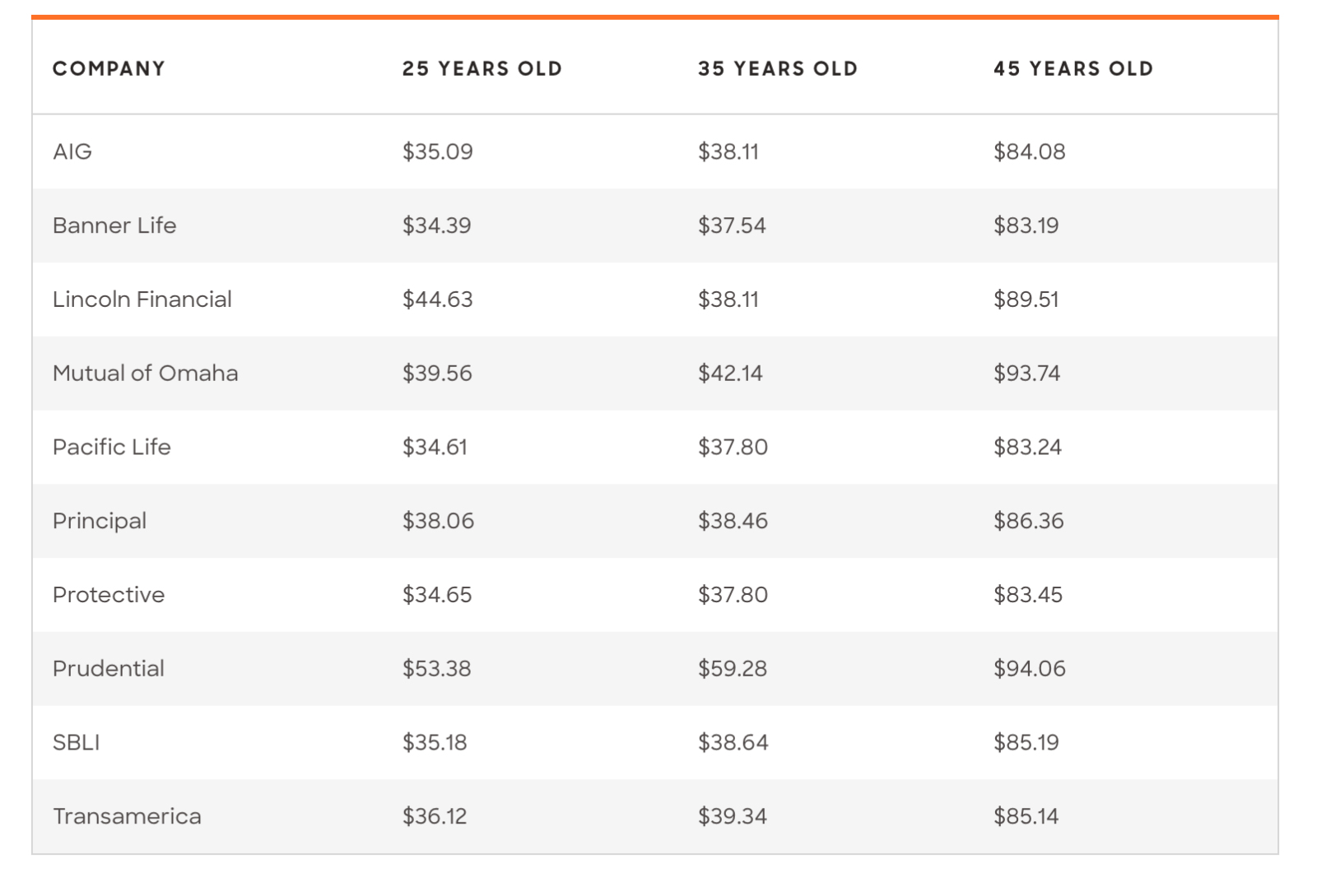

Overpriced Compared to the Competition

In today's day and age, consumers want to purchase whole life insurance that fits into their budget. For this reason, they shop for a policy based on many factors, with price often at the top of the list.

Sagicor struggles in this area, as its whole life coverage is traditionally priced higher than the competition. For this reason, consumers are often able to find a lower priced policy from another company, all without giving up anything in terms of coverage or additional features.

No Dividend

One of the primary benefits of purchasing whole life insurance is the ability to earn a dividend, thus increasing the cash value of your policy.

Unfortunately, Sagicor does not pay out a dividend at this time.

Once again, this puts the company at a disadvantage when compared to providers that have a history of paying a dividend to policyholders.

Since most consumers are interested in a policy that earns money over time, Sagicor shoots itself in the foot by neglecting to pay a dividend.

Long Underwriting Process

Sagicor has a different underwriting process for each type of policy, such as:

- Fully Underwritten Process

- Accelewriting Process

- Juvenile Issue Process

While there is nothing wrong with this approach, many consumers find that the underwriting process takes entirely too much time. As a result, they have to wait around to receive an approval (or denial) and for their policy to be active.

Final Word

You always need to keep an open mind when shopping for whole life insurance. Even so, there are some details that you can't afford to compromise on.

Unfortunately for Sagicor, many consumers consider the premium and dividend payment to be among the most important details.

Sagicor may be worth a second look, but don't purchase from this company until you first see what the competition has to offer. It's likely that you'll find a provider with a great reputation, a lower price, and a dividend.

Check out some of our other reviews: penn mutual whole life insurance review, ohio national whole life insurance review, state farm whole life insurance review & More...