Whole Life Insurance Quotes Online (2026)

Updated July 6, 2026

Quick answer: Get whole life insurance quotes online instantly — compare A+ rated mutual carriers in about 60 seconds. Real whole life premiums, not term-only results.

Most online quote tools show term life even when you search for whole life. Top Whole Life compares permanent whole life from multiple carriers in one place.

Before You Buy

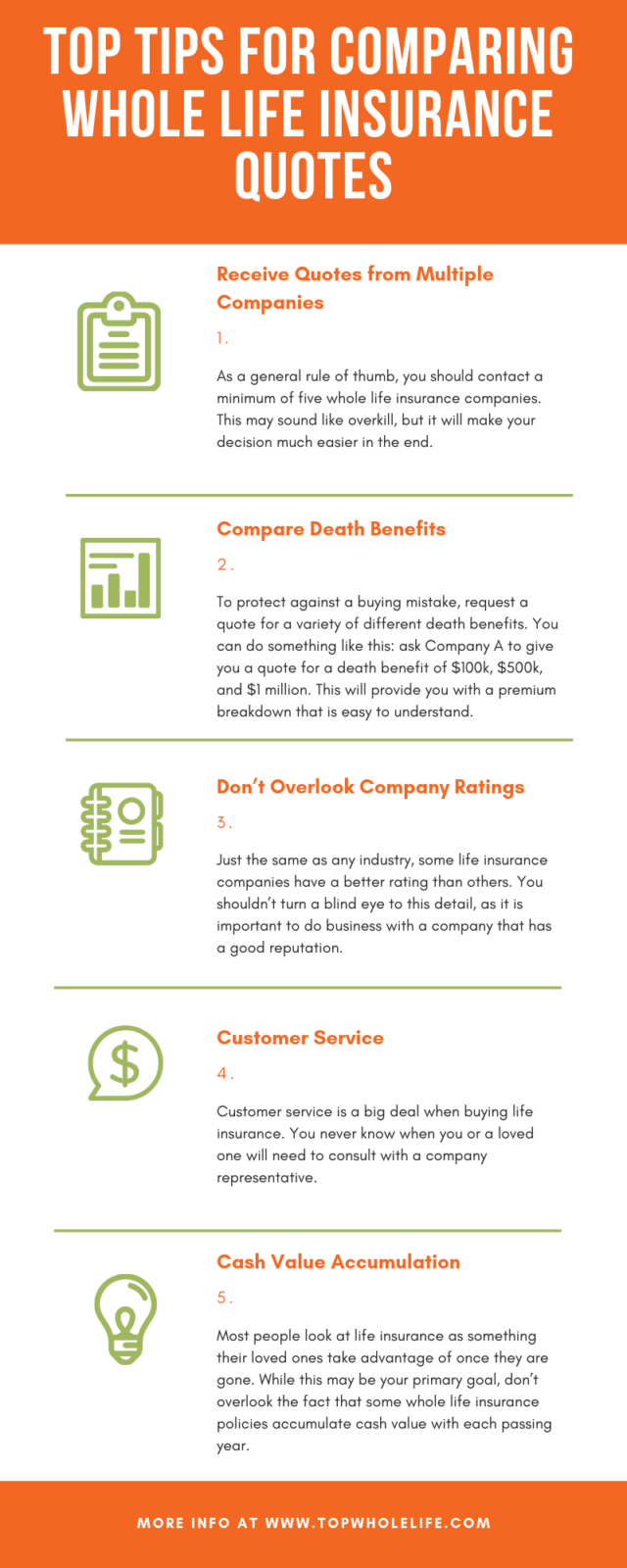

Compare quotes from different insurers before choosing whole life, term, or universal life. We routinely see 30%+ premium differences and 60%+ cash value growth differences between carriers for the same applicant.

Evaluate: whole life cost FAQs, top 7 carriers for cash value, death benefit, dividend history (rate chart), and AM Best ratings.

The Problem With Whole Life Insurance Quotes Online

Term quote engines (Term4Sale, Rootfin) are everywhere. Whole life quote engines are not.

Search for "whole life insurance quotes online" and most results lead to:

- Term-only comparison sites

- Burial/final expense policies ($2,000–$25,000), not full whole life

- GUL or IUL quotes mislabeled as whole life

Calling each carrier individually means multiple agents, conflicting advice, and 20-page illustrations that are hard to compare.

The Solution: Compare Whole Life Quotes Online

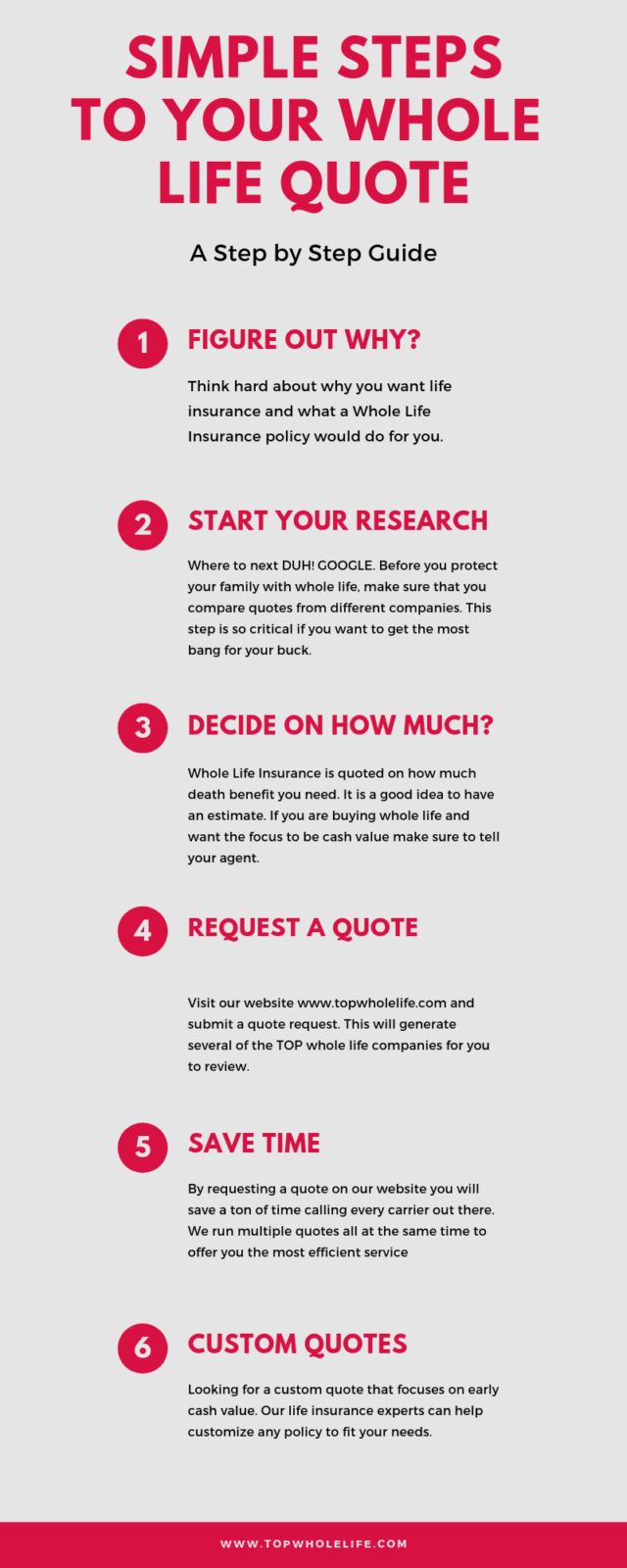

We built Top Whole Life so informed buyers can compare whole life quotes online from A+ rated mutual carriers in about one minute.

Get your free whole life quote →

Our tool shows side-by-side premiums from participating whole life insurers. When you are ready to apply, our team walks you through underwriting by phone — contact us anytime.

For cash-value-focused buyers, start with our top 7 whole life companies ranking before you quote.

Save Time and Energy

Instead of calling MassMutual, State Farm, Northwestern Mutual, and New York Life separately, run one comparison:

Why Our Online Quotes Are Different

Unlike generic insurance sites, we quote whole life specifically — same product type, comparable death benefits, mutual carrier focus. You enter basic info (age, gender, coverage, state) and see real whole life rates, not term bait-and-switch.

Explore related guides: compare whole life quotes step by step and our cost calculator intro.