Life Insurance Pricing 101: Unveiling the Truth Behind the Numbers

When it comes to protecting your loved ones and securing their financial future, life insurance plays a crucial role. However, many people are unsure about how much life insurance they need and how the pricing is determined. In this article, we will delve into the world of life insurance pricing and unveil the truth behind the numbers.

Understanding Life Insurance Pricing

Life insurance pricing is based on several factors that determine the risk associated with insuring an individual. The main factors that influence the cost of life insurance include:

Age: The younger you are, the lower the cost of life insurance. This is because younger individuals are generally considered to be healthier and have a longer life expectancy.

Gender: Women tend to have a longer life expectancy compared to men, which means they typically pay lower premiums for life insurance.

Health and Medical History: Your overall health and medical history play a significant role in determining the cost of life insurance. Insurance companies will assess factors such as pre-existing conditions, family medical history, and lifestyle choices (such as smoking or excessive alcohol consumption) to determine your risk level.

Coverage Amount: The amount of coverage you choose will also impact the cost of your life insurance policy. Generally, the higher the coverage amount, the higher the premium.

Policy Type: There are different types of life insurance policies, including term life insurance and whole life insurance. Term life insurance offers coverage for a specific period, while whole life insurance provides coverage for your entire life. Whole life insurance tends to be more expensive due to its lifelong coverage and the accumulation of cash value.

Calculating the Cost of Life Insurance

To determine how much life insurance you need and the associated cost, it's important to consider your financial obligations and goals. Here are some steps to help you calculate the cost of life insurance:

Evaluate Your Financial Needs: Determine how much money your loved ones would need to maintain their current lifestyle and cover expenses such as mortgage payments, education costs, and daily living expenses.

Assess Your Existing Assets: Take into account any existing savings, investments, or other sources of income that could help support your family in the event of your passing.

Consider Future Expenses: Anticipate any future financial obligations, such as college tuition for your children or outstanding debts that would need to be paid off.

Secure your future today. Get the truth on life insurance pricing!

Click below to get a Quote Now!

Consult with an Insurance Professional: Work with an experienced insurance agent or financial advisor who can help you assess your needs and recommend the appropriate coverage amount.

Get Quotes from Multiple Insurance Companies: Shop around and compare quotes from different insurance companies to ensure you are getting the best coverage at the most competitive price.

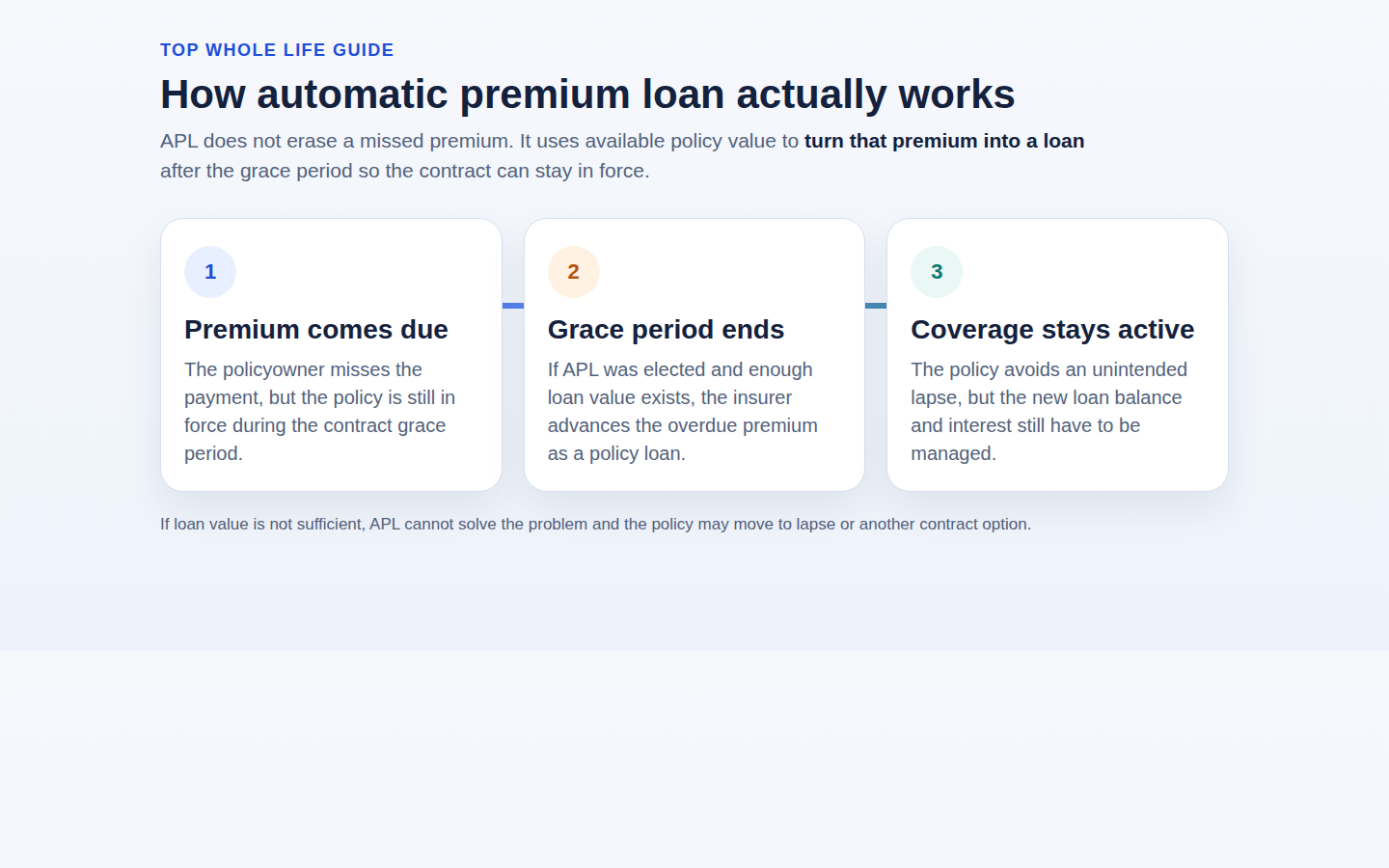

The Benefits of Borrowing Against Your Whole Life Insurance Policy

One of the unique features of whole life insurance is the ability to borrow against the cash value of the policy. Here are some benefits of borrowing against your whole life insurance policy:

Access to Cash: By borrowing against your policy, you can access funds for various purposes, such as paying off debt, covering medical expenses, or funding a business venture.

Lower Interest Rates: Borrowing against your whole life insurance policy often comes with lower interest rates compared to traditional loans or credit cards.

No Credit Checks: Since you are borrowing against your own policy, there is no need for credit checks or extensive paperwork.

Tax Advantages: The cash value of a whole life insurance policy grows on a tax-deferred basis. When you borrow against the policy, the loan is not considered taxable income.

Flexibility: You have the flexibility to repay the loan on your own terms, without any strict repayment schedule.

It's important to note that borrowing against your whole life insurance policy reduces the death benefit, and any outstanding loan balance at the time of your passing will be deducted from the payout to your beneficiaries. Therefore, careful consideration should be given before utilizing this feature.

Conclusion

Understanding the factors that influence life insurance pricing and how to calculate the cost of coverage is essential for making informed decisions about your financial future. By evaluating your needs, consulting with professionals, and comparing quotes from different insurance companies, you can find the right life insurance policy that provides the necessary protection for your loved ones. Additionally, the ability to borrow against the cash value of a [whole life insurance policy]our quote tool can provide financial flexibility and access to funds when needed. Remember to carefully weigh the pros and cons before utilizing this feature.