Key Man Life Insurance | Expert Tips To Protect Your Key Employees

Key Man Life Insurance

In the following article, we will go over key man life insurance strategies. We will review policies and all the information you need to protect your key employees. If all you are looking for is a quote, contact us at (mailto:quotes@topwholelife.com).

Also, we will go over all the different insurance types to find out which insurance may be a better fit for you. Then, we will clarify which is better Term Insurance, Whole Life Insurance, or Universal when protecting a business against the loss of a Key Man and/or Owner.

Key Man Protection

The death of a key man presents tremendous problems for a business. Some of the potential problems are:

Income Continuation

- How will the deceased key man's family be able to replace his salary?

- Will the business afford to pay his/her family without being there to contribute to the business's profitability?

Key Management Loss

- What will the impact be on day-to-day operations, sales, profits, growth, working capital, and relationships?

- Who will take care of the roles and responsibilities?

The death of a business owner compounds the problems.

Income Continuation For The Business

- How will the owner's family be able to continue his salary, as well as the employee's salary?

- Will the business survive?

- Which family members will be involved in the business?

- Which family members will control and manage the business?

All of the previous examples point to why Key Man Life Insurance is a critical component for any business.

How Do You Design A Policy To Protect A Key Man?

In reality, there are multiple ways to protect a key man. Selective compensation plans are additional ways to create a fortune for key men and business owners.

Key Man Bonus Plan

The corporation pays the premium on a policy of which the key man is the owner. This is treated as a bonus to the executive and is deductible by the corporation and taxable to the executive. The executive's cost is the tax on the bonus. The executive is the owner of the policy, and his family is the beneficiary. Assuming the executive lives until retirement, he then supplements his retirement income by withdrawing money from the cash value.

Split-Dollar

An agreement between the corporation and the key man wherein the corporation pays the premium on a policy. The corporation recaptures its payments from the cash value or the death benefit when the key man dies. The key man's cost is that he pays tax on the term cost for the insurance. Additionally, the Cash Value can be used to pay supplemental retirement benefits to the key man.

Supplemental Executive Retirement Plan (SERP)

The corporation is the owner and beneficiary of the policy on the key man. If a key man dies before retirement, the corporation uses a portion of the death benefit to pay salary continuation to the key man's family. Assuming the key man lives until retirement, the company pays substantial retirement benefits to the key man, using the cash value or other corporate cash assets, and then recaptures its cost from the policy when the key man dies. The number of variations of these plans is virtually unlimited for business owners.

Key Man Life Insurance Types

There are multiple different kinds of insurance you could pick to get a key man life insurance policy. We go over the most common ways to protect your key employees.

Whole Life Insurance for Key Man: Puts the "Life" in Insurance

At first glance, many people do not see the advantages of owning a whole-life policy. They see a high premium, as compared to a relatively low premium for term life insurance. But ask yourself, why would a company be willing to give me $1 million of coverage for an annual premium of only $800 a year for twenty years while the same company is charging an annual premium of $12,000 for a whole-life policy? Before you answer, read on.

What costs more, a bag of gold or a bag of sand?

Insurance companies know that their term-life policies will not result in many death claims. Of the millions of term-life insurance policies sold, fewer than five percent will result in a death benefit being paid. Most policies either expire or lapse.

The only way you can win with term-life insurance is to die young, and that is not a scenario that any of us would actually call winning. If you outlive the policy- and you most likely will- you lose, and you will lose a substantial amount of money.

Benefits Of Key Man Life Insurance With Whole Life

The benefits of whole life insurance include the following:

- The premium is guaranteed. Whole-life insurance has a guaranteed level premium for the life of the policy. It does not change over time, and you never have to worry about an increase in premium due to poor health, interest rates, or stock market conditions.

- The premium consists of a guaranteed "cash value" as well as a death benefit. Only a small portion of the premium in a whole-life policy represents the "cost of insurance." Most of the premium consists of your savings, called cash value. So the whole life is both an insurance and a savings vehicle. Term-life insurance does not have the savings feature; it only has the insurance cost. The savings feature makes whole life an essential financial tool and one you should seriously consider.

- Cash value accrues tax-advantaged. The cash value increases, tax-free, until the policy's cash values are greater than the total premium paid. At that point, the cash value in the policy grows on a tax-deferred basis. When a death occurs, all of the policy's cash values are an income-tax-free benefit no matter how much the gain over the premium paid.

- The whole-life policy also pays a dividend. Once a year, a traditional whole-life policy declares a dividend. The amount of the annual dividend from year to year is unknown, and paying the dividend is done at the insurance company's discretion. But when the policy is sold, the company makes a projection of these dividends based upon its current financial position. Therefore, the dividend is technically not "guaranteed"; it could be higher or lower than what the company projected for that year.

Other Advantages Of Key Man Life Insurance With Whole Life

Most insurance companies have paid dividends consistently for over 100 years. Remember that once a dividend has been paid to you, it cannot be lost or taken away; it is guaranteed to remain. That is unlike dividends on investments, which can be lost due to future market declines if they are reinvested in the investment.

- The insurance company can pay premiums for you if you become disabled. Although you must pay a small amount of extra premium for it, the disability-waiver-of-premium rider is well worth having. With this rider, should you become disabled, the insurance company will continue to pay the full premium for you. Since most of the premium is actual cash value, the cash value and any dividends/interest will continue to build up to help you meet any future savings needs, such as college education for your children or your own retirement income.

- Whole life provides wide flexibility. You can use your dividends in many different ways. To me, one of the best ways to use the dividends is to have them purchase additional paid-up insurance, which increases the policy's death benefit over time. This helps fight inflation, compared with the death benefit of a term policy, which remains level or even declines over time.

Advanced Strategies For Key Man Life Insurance With Whole Life

But should you need to, you can also take the dividend in the form of cash each year. You can use the dividend to supplement your income, to invest, or pay down any debt you might have. You can also use your dividend to pay the policy's premium; as time goes by, the dividend may be large enough to pay the entire premium.

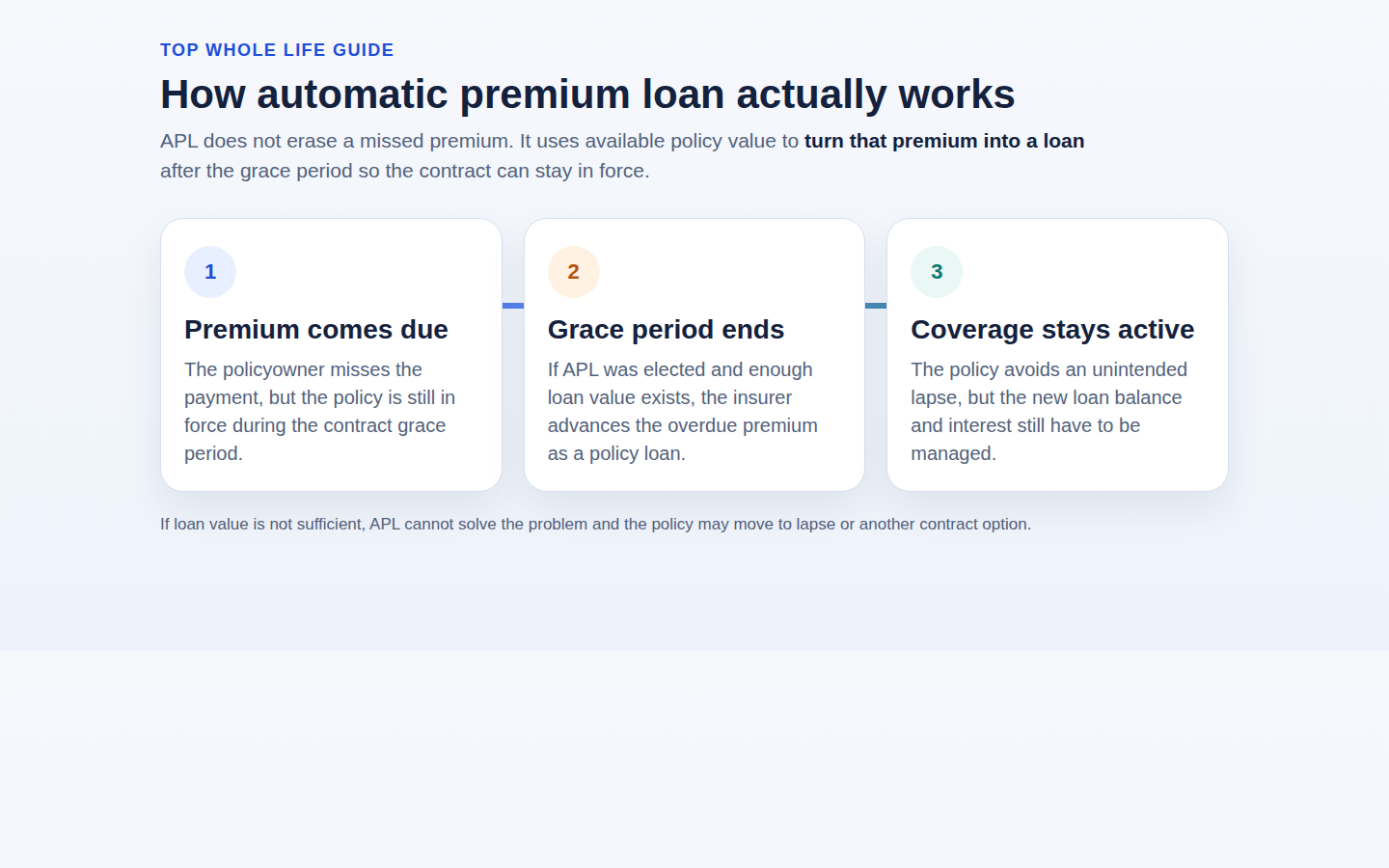

You can borrow money from your policy.

You don't have to surrender a policy to access your cash value. The "policy loan" provision allows you to borrow up the amount of cash value. Unlike other kinds of loans, you never have to pay this loan back, as long as you keep paying the premium and the current interest on the loan. The loan only has to be paid off at the time of death, from the proceeds of any death benefit paid out to your beneficiaries.

Borrowing Can Be Miss-Understood

One thing I want to make clear here is that you are not borrowing your own money. Many financial writers and advisors erroneously claim that you are borrowing, and therefore, you should not be paying any interest. This is untrue. It is not your money you are borrowing; you cannot be your own banker. When you borrow against an insurance policy's cash value, you are actually borrowing money from the insurance company and allowing the insurance company to hold your cash value intact as collateral for the loan.

- You can also use your cash value as collateral for a bank loan. Banks will normally loan close to 100 percent on the cash value and dividends in the account on a favorable basis.

- The cash value is exempt from creditors. This is a little-known but significant benefit of whole life insurance. In most states, life insurance cash value is not exposed to liability judgment. Check with your insurance company to see if this is true in your state.

In summary, when you take into account all of the benefits of growth in guaranteed cash value, declared dividends, income tax savings, avoiding costly term-insurance premiums, and the high overall rate of return over a period of time, it isn't easy to find a savings vehicle that has consistently returned more money than whole life insurance.

Lower Risk Option

Also, you will have peace of mind because of the lower risk involved in whole-life insurance. So it is nearly impossible to have a more effective and efficient way to build and protect your wealth.

The only significant disadvantage to whole-life insurance is that it is not a short-term financial project. Whole life is a lifelong financial product that acts as one of the pillars of your wealth-building process. The cash value does not really begin to build up until the policy has been in force for a couple of years. Whole-life insurance is definitely a long-term insurance product and should not be considered if you are making a short-term purchase.

Key Man Term Life Insurance

Term insurance has a place in many people's life insurance portfolios. It is the opposite of the whole life. It builds no cash value; its death benefit stays level or declines; it is for the short term rather than the long term, and it will most likely "run out of" death benefit by lapsing or expiring.

Most people consider term insurance because it is inexpensive. It is inexpensive because it only provides a death benefit and only for a specified time. For this reason, it should be used only in a specific short-term need for a death benefit and not as part of a serious long-term financial or estate plan.

Whenever buying an individual term insurance policy, you should always seek to buy convertible insurance. Buying convertible term life at an early age guarantees insurability later, even if your health deteriorates. Whenever possible, you should seek to convert term life to whole-life insurance as soon as you can afford to do so.

Universal Life Insurance For Key Man

Universal life typically has a lower premium than whole life and flexibility of premium payments. This affords you more death benefit for the same premium as your whole life while allowing you to adjust your premium to suit a changing budget.

Universal life pays a straights interest rate on the cash value in the annuity portion of the policy. The interest rate changes annually or semiannually, depending on the policy. The lack of a dividend is a disadvantage of universal life. Another disadvantage is that interest cannot be removed tax-free if you wish to take a cash interest.

Although some universal life offers a disability waiver of premium, this waiver in many cases is only on the pure protection portion of the policy. The cash value does not increase from that point on. If you choose to pay a lower premium, this can reduce the ultimate death benefit and even risk policy lapse if the interest rate declines.

Not For Cash Value

You should only consider a Universal Life when all you want is to have a death benefit for key man insurance purposes.

This is not an appropriate insurance policy for retirement planning, estate planning, income tax strategies, or charitable giving. It would help if you used universal life insurance because the death benefit can fluctuate, and the tax benefits are not as advantageous as with whole life.

Also, universal life policies should be viewed as more appropriate than term insurance as a long-term death benefit. But it is not as appropriate to use as whole-life insurance for more permanent needs or cash value accumulation or distribution.

Suppose you think of whole life as a luxury car, universal life as a mid-size car, and term life as an economy car. We know this analogy is not completely accurate, but it is useful to understand the differences among these products. They offer different advantages and disadvantages, and the price difference should not be the only factor in deciding which to purchase.

Also, you should be aware that there a Universal Life policy that is guaranteed to payout. These are usually called guaranteed universal life policies or no-lapse universal life policies.

Variable Life Insurance For A Key Man

Like universal life, variable life insurance is a combination of term insurance and an annuity. However, instead of a straight interest-payment annuity, with variable life, you have a choice of how to invest the cash value among many different "sub-accounts," which are essentially mutual funds.

Be Careful With The Variable Part

This "investment" of cash value rather than the "saving" of cash value offers the possibility of increasing the cash value above what a universal-life or whole-life policy could offer. But it also puts the cash value at risk. Another disadvantage is that there are no dividends, and you must borrow to get money out of the policy. If you borrow from the policy and the stock market declines simultaneously, you may experience more premium "calls," or a loss of death benefits, or the policy may even lapse.

You probably shouldn't consider variable life insurance for a key employee because it is not appropriate for retirement planning, estate planning, income-tax strategies, or charitable giving. The main reason is that the growth of its cash value is not secure or guaranteed. Therefore, the policy's success is strictly a matter of chance in the markets, and you take all of the risks.

I Want To Get A Key Man Life Insurance

The first step is to get a FREE consultation to ensure you or an employee needs life insurance.

Our experts will help you determine what type of policy you should get and what type of advanced strategy you should use. The process can seem long, but our experts will give you all of your options, and we will do it quickly and efficiently.