Is Life Insurance Taxable? | Top whole Life

Life insurance is one of the most important types of insurance that you can have. After, all it can provide peace of mind for you and your family when the inevitable happens.

If you already have a life insurance policy in place you may have questions about your tax responsibility. A common question that policyholders like to know is, "Is life insurance taxable?"

To help you have a better sense of how the taxes on life insurance work, we've created this article, where you will learn all about life insurance and taxes.

What Is Life Insurance?

Life insurance provides money to your loved ones once you have passed away. It provides a lump sum of money, to a beneficiary that you name.

You are able to choose between whole life insurance to protect your familys future that covers your entire life. Or you can choose a term life policy that protects your life for a particular term. You are also able to How To Choose The Right Amount Of Life Insurance (consumerreports.org) on the policy, which will determine your monthly premiums.

At the time of your death, your beneficiary can file a claim with the insurance company, and the life insurance payout process will begin. Life insurance can be for final and future expenses. Those expenses include:

- Funeral costs

- Mortgage payments

- Children's college funds

- Medical Bills

- Credit Card Debt

- Loans

Is Life Insurance Taxable?

Having an understanding of what life insurance is will also allow you to understand why it is tax-free. According to the IRS, any life insurance benefits that you receive as a beneficiary in the event the insured has died are not taxable. The reason being the benefits aren't included in your gross earned income.

You aren't required to report any life insurance proceeds that you received. While the initial proceeds from a life insurance policy are not taxed, any interest earned from the money is subject to taxation. You also want to ensure that you report the interest earned as well.

Is Your Life Insurance Premium Taxable?

To keep a life insurance policy enforced you may choose to pay a monthly or single premium. In general life insurance premiums are not taxed. They are also not subject to sales tax either. It is equally important to note that your life insurance premiums are also not tax-deductible.

In most situations, life insurance premiums aren't taxed. Yet there are a few situations where a policyholder could be responsible for paying taxes on their policy. We'll explain this later in the article.

Is the Cash Value on Your Life Insurance Taxable?

There are a few instances when the cash value on your life insurance would be taxable. This could happen if you decided to sell or surrender your policy.

Before you decide to sell your life insurance policy may want to consider selling it. If you sell your life insurance policy you can potentially walk away with more money.

This option is commonly referred to as a life settlement. The reason you may get more money from selling a policy is that the price you sale your life insurance policy for is not determined by its cash amount.

Rather, it's based on your life expectancy, your premium amounts, and the death benefit. When selling a life insurance policy the IRS can levy two types of taxes.

The first tax is income tax, which is any proceeds that exceed your policy basis. The other type of tax is capital gains. This is taxes on any proceeds that exceed the cash value of the policy.

Your other option would be to surrender your life insurance possible for the accumulated cash value. Any portion of the cash value that is over the policy basis is taxable.

An example would be if you surrendered a policy for $30,000. If the policy basis was only $15,000, the IRS would tax the other $15,000 as it counted as additional income.

If you are looking to get out of your current life insurance policy you can buy a different one. It could be beneficial for you to trade your policy by way of 1035 exchange.

This special provision in the United States tax code will allow you to exchange your life insurance policy for another one. You can do this without having to pay any capital gains tax.

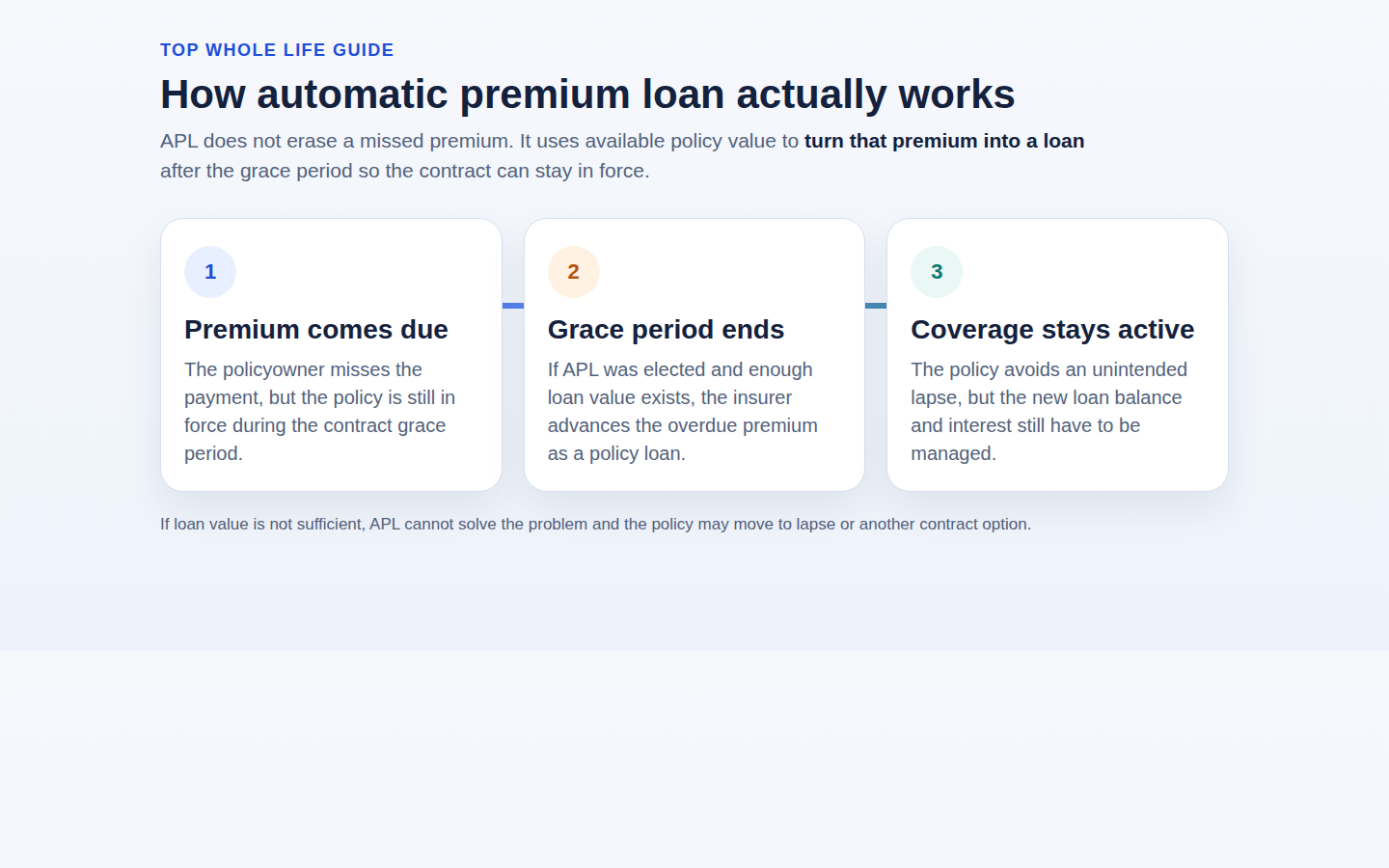

Taxes on Life Insurance Loans

One last thing to note when it comes to taxes on cash value is if you take out a loan against it. When it comes to a borrowing from a life insurance policy on the cash value is tax-deferred. What this means that you are able to borrow cash on a tax-free basis but you will have to pay it back.

If you do not pay the loan back you will be subjected to hefty tax implications. For example, if you had a policy with $20000 in cash value. Let's say your loan basis was $10,000. This would mean you have paid $5000 in premiums.

If you were to take out a $6000 loan, you won't have to pay taxes on the $14000, while the policy is active. The important thing to remember is your loan is accruing interest. When the amount you own becomes greater than the cash value that is where the problem lies.

If it comes to that point you have to repay the loan or your policy can get canceled by the insurer. If the insurer cancels the policy they will use the cash value to repay the loan and you have to pay the taxes on the amount that exceeds the policy basis.

Is the Life Insurance Payout Taxable?

With life insurance, the lump sum payout of the death benefit is not taxable. What this means is your beneficiary doesn't pay taxes on the life insurance payout.

Yet, as mentioned before, there can be some rare exceptions to this rule. The life insurance payout may be subjected to taxes if the beneficiary receives the benefits in installments.

This situation can arise when the insurer holds the principal amount in an account that earns interest and issues the death benefit over a fixed amount of years. The interest that the death benefit accumulates will be taxed.

Another way the life insurance payout can become taxable if it becomes apart of your estate. There is a federal estate tax exemption limit called the lifetime gift tax. The amount of that limit is $11.58 million dollars.

What this means is that if your estate has a total value that is greater than this amount the IRS will levy an estate tax. It is important to note that any life insurance policy paid out when you die is included in the payout to your estate.

So if your policy pushes you over the $11.58 million thresholds your estate will owe taxes. To avoid this you can transfer the ownership of the policy to someone other than yourself before you pass.

There is a three-year rule, with this. The rule states a policy is still considered part of your estate if a transfer of ownership occurs within three years of your death.

You also want to know that depending on the ownership of the policy there are taxes called a gift tax. For example, if you were to buy a policy to provide death benefits on your spouse and your child is the beneficiary the IRS considers this a gift.

In this case, as the policy owner, you are the donor and could be liable to pay a gift tax.

Is Group Term Life Insurance Taxable?

There are instances where your Group Term Life Insurance (IRS) can be taxable.

If your employer-provided a life insurance policy as a part of your compensation plan. In this example, the IRS would consider this income, and thus you the employee would be required to pay taxes.

Yet the taxes that you would be responsible for would only apply if your employer paid more than $50,000 in coverage for your life insurance policy. It is important to note that if the policy is over $50,000 in coverage the first $50,000 would be exempt from taxation.

You would be responsible for covering the taxes for anything over the $50,000 threshold.

If your life insurance coverage was rolled into your salary, retirement plan, and health benefits, you wouldn't be subjected to taxes. That's because at that point it would not exceed the limit amounts placed by the IRS.

Here to Meet Your Life Insurance Needs!

Answering questions like, "Is life insurance taxable?" can be difficult to answer by yourself. Yet, you don't have to do this alone.

If you still have questions about your life insurance options and how taxes can affect them, contact us!