Compare Whole Life Insurance Quotes (2026)

Updated July 23, 2026

Quick answer: Use the quote form above to compare whole life insurance quotes from A+ rated carriers in about 60 seconds — side-by-side premiums, death benefit, and carrier strength. Use the term vs whole matrix to confirm you are shopping permanent coverage, not term-only engines.

For cash value rankings, see our top 7 whole life companies guide.

Understand Different Types of Life Insurance

The two main types are term life and permanent life (whole life, universal life, etc.).

| Term | Whole life | |

|---|---|---|

| Duration | Fixed term (often 10–30 years) | Lifetime (if premiums paid) |

| Cash value | No | Yes (scheduled + possible dividends) |

| Premium pattern | Usually lower initially; renewals can jump | Typically level for life on traditional designs |

| Best for | Temporary income replacement | Lifelong protection + long-term asset |

If you want permanent coverage with cash value, focus on whole life quotes — not term comparison sites that dominate search results. Related: whole life insurance quotes online.

Coverage Checklist (before you compare)

Use this quick checklist, then enter face amount in the form above:

- Income replacement (often 10–15× annual income as a starting point)

- Mortgage / debts you want paid off

- College or dependent costs

- Final expenses and estate liquidity

- Preference for cash value / dividends vs. cheapest temporary premium

For high face amounts, see $1 million whole life cost.

Also weigh cash value growth and dividends — our dividend rate history pillar tracks mutual carrier performance over time.

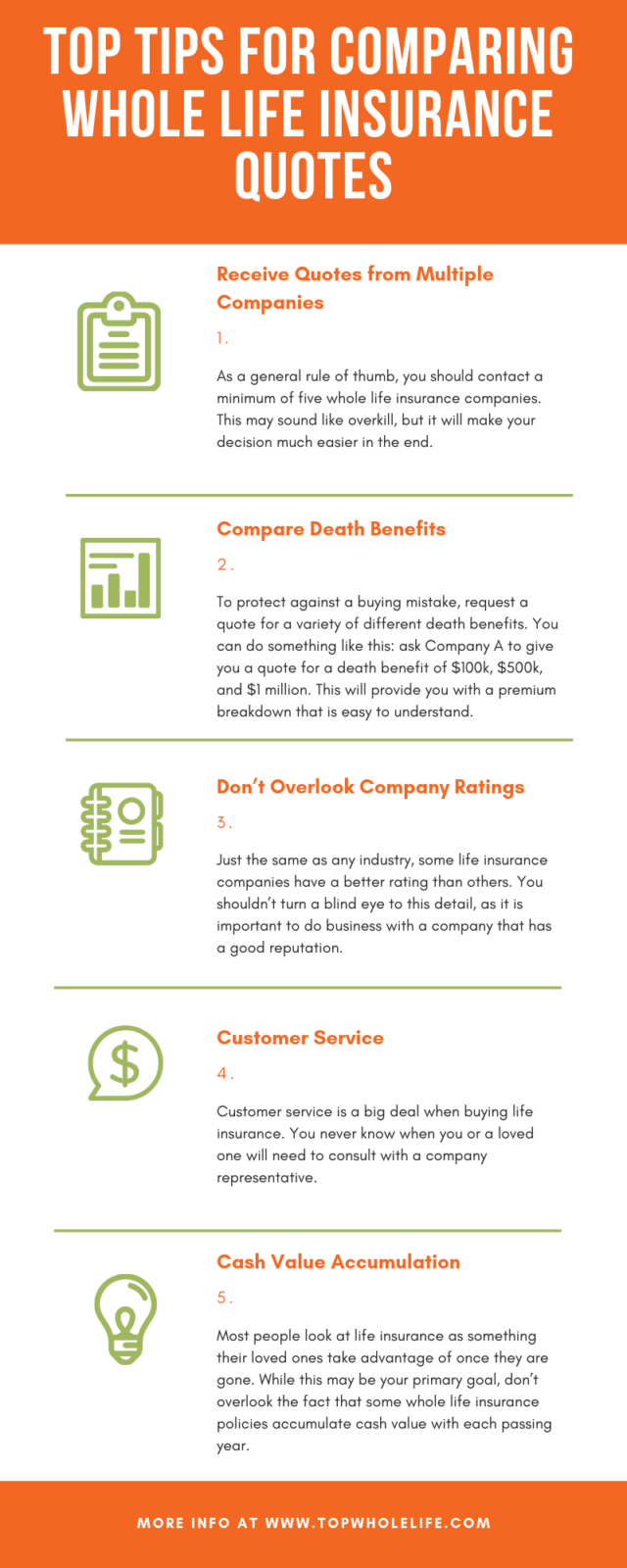

What to Compare Across Carriers

When quotes return, look at more than first-year premium:

- Premium for the same death benefit and similar pay period

- Cash value illustration (years 10, 20, 30)

- Dividend history (participating whole life)

- Financial strength (AM Best, Comdex)

- Riders and underwriting class assumptions

Our top 7 whole life insurance companies for cash value ranks MassMutual, Penn Mutual, New York Life, Guardian, and others on these factors.

Riders and Fine Print

Common riders include waiver of premium (disability), guaranteed insurability, and accelerated death benefit for terminal illness. Factor rider cost into your comparison — a lower base premium is not always the better value.

Review exclusions (suicide clause, contestability period) and how cash value loans / surrenders work. Whole life is a long-term contract.

Work With a Trusted Expert

A licensed whole life specialist can explain illustrations and match you to the right carrier. Start with the form at the top of this page, then contact us if you want a guided comparison.

In Conclusion

Compare whole life quotes by coverage need, carrier financial strength, cash value design, and total cost — not premium alone. Use the on-page tool above to compare A+ rated carriers in about 60 seconds.