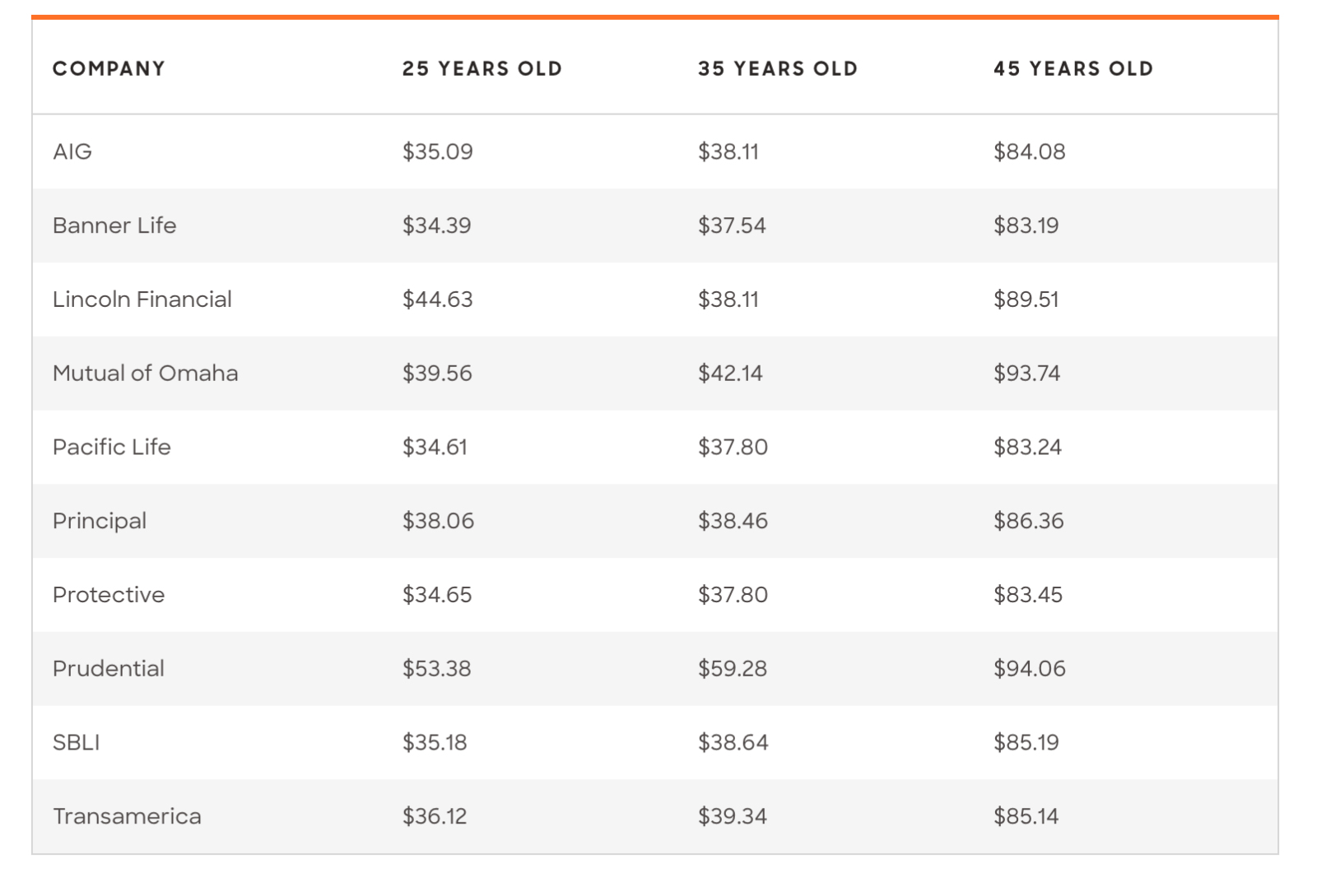

LadderLife Affordable Life Insurance for Seniors – Comprehensive Review

Ladder Life Insurance Review

Life insurance is an important product that everyone should have, but it can prove hard to find the right affordable coverage.

Ladder life insurance company is a relatively new provider. The company offers insurance products in the United States.

Its product isn't one of the best options for consumers. Still, we'll give you a brief overview of what they have to offer.

Keep reading for an overview of Ladder life insurance.

An Overview of Ladder Life Insurance

Ladder life insurance is a mid-level provider. The underwriter offers term life insurance across the nation.

You can sign up for Ladder life insurance using their online application. Many Ladder life insurance policyholders don't need to take a medical exam. They sell policies to adults between the ages of 20 and 60.

Ladder life insurance is a startup insurance company. They've been in business since 2015. Since then, the firm has expanded across the United States.

The company's partnered with the SoFi personal finance company. It also has business dealings with NetLaw.

Ladder life insurance receives average marks for performance. Part of the company's median rating comes from consumer complaints.

There's a meaning behind the company's name. In fact, it's part of the Ladder life insurance marketing angle.

The insurer allows policyholders to adjust their coverage as needed. This practice is called laddering.

It's an insurance ladder that allows you to raise or lower coverage when desired. This practice is where the company gets its name.

Insurance laddering is much more convenient than canceling your existing life insurance and applying for a new policy. For instance, a policyholder's child might graduate from college. Alternatively, a policyholder might pay off their mortgage.

In these instances, a Ladder customer can reduce their coverage because it's no longer needed. In turn, it's a way to save money by not spending on unnecessary life insurance.

Available Ladder Life Policies

With this in mind, Ladder claims that it enables consumers to save thousands of dollars over the years by letting them adjust coverage.

The firm is more like a tech company in the insurance business. They offer customers a streamlined online experience.

Ladder sells all policies online without the help of agents. They also provide some applicants with instant decisions. In some cases, Ladder applicants can receive coverage minutes after applying.

The underwriter offers policies of up to $8 million in coverage. This maximum limit is significantly high compared to other term life underwriters. In addition, the policies provide coverage that ranges from 10- to 30-year terms in increments of five years.

However, the company only offers one kind of insurance product€”term life insurance.

Ladder Term Life

Ladder offers a level-term life policy. In other words, your rate will not change for the entire term length.

Term life is one of the easiest kinds of life insurance policies to acquire. It's also the most affordable kind of coverage.

However, term life is a limited product. It's temporary life insurance.

Permanent life insurance might better life insurance loan borrowing money from your life insurance policy. However, some policyholders at least want coverage into their older years. If you fall into this category, you may want to consider a whole or universal life policy instead.

Insurance Rider Options

A conversion rider is optional add-on insurance for insurance coverage. When you buy a rider, it's added to your life insurance policy.

Insurance riders can provide you with a range of value-added benefits. For example, you may need to purchase additional coverage for your spouse. In other cases, you might want to purchase life insurance coverage for your children.

Otherwise, you may want accelerated death benefits. With this kind of rider, you'll receive compensation in the event a physician diagnoses you with a terminal illness.

Ladder life insurance does not offer riders. Accordingly, the company's life insurance policies don't allow you to access extra protection for your family or yourself to cover financial obligations.

Applying for Ladder Life Insurance

Applying for Ladder life insurance is straightforward. Again, the entire application process takes place online. In most instances, it may take you about five minutes to complete the application.

The underwriter will then inform you whether your application was approved or denied. Alternatively, they may ask you for more information.

Typically, this information includes facts about your health. Often, Ladder will send a lab kit to applicants if the company wants to know more about their physical condition.

Ladder processes the lab kit free of charge. This practice also allows you to avoid scheduling an in-person doctor's visit.

Laddering with Ladder Insurance

The biggest feature of Ladder life insurance is the ability to adjust coverage as needed. For instance, you may welcome a new addition to the family. In that case, you may want to increase your coverage by adding your child to your life insurance coverage.

Alternatively, you may need less life insurance for some reason. In that case, the company allows you to decrease your premiums proportionately to your coverage.

For instance, you may pay a $30 per month premium for $500,000 of coverage. However, with laddering, you might reduce your coverage to $400,000 and only pay $24 per month.

Company Reputation

The National Association of Insurance Commissioners (NAIC) scrutinizes complaints in the insurance industry. The NAIC first takes market share and collected premiums into account when assessing the acceptable number of complaints. Next, the association uses this information to estimate how many complaints an insurer should receive. Finally, it compares these points to how many complaints were filed against a company.

The average number of complaints against an insurer is always 1.00, according to NAIC standards. If a company ranks lower than 1.00, it received fewer complaints than the industry standard. If an underwriter receives a rating higher than 1.00, they've received more complaints compared to what's normal for the industry.

Two companies issue Ladder life insurance policies. One company is Cis Refined Results (NAIC) Company of New York. The other company is Fidelity Security Life Insurance Company.

Allianz Life Insurance Company of New York had a complaint index rating of 0.25 in 2020. Meanwhile, Cis Refined Results (NAIC) Insurance Company had a complaint index rating of 0.31.

The Ladder Life Insurance Website

The Ladder Life Insurance site is mobile-friendly and well-designed. What's more, the online insurance quote process is fast.

The site also offers life insurance education. You can also access the Ladder calculator. With it, you can use it to figure out your coverage needs.

You can also download the free Ladder mobile app. The app also lets you apply for coverage. You can also use the app to increase or decrease your coverage as desired.

Again, however, Ladder life insurance only sells term life. As a result, there's no option to save on your insurance premiums by bundling other insurance products, such as home or health policies.

Benefits and Drawbacks of Ladder Life Insurance

Ladder Life has both pros and cons. One positive about Ladder life insurance is that the application process is straightforward. Also, as previously mentioned, the companies that issue Ladder products receive relatively few consumer complaints.

Ladder Life Benefits

The range limit for Ladder life insurance coverage starts at $100,000. It maxes out at $8 million. You can adjust your coverage between these two amounts during the time your policy is active.

Ladder's $8 million maximum limit is impressive. Most companies require a medical exam for coverage over $3 million. However, not everyone qualifies for a no-medical exam policy.

What's more, the company lives up to its namesake by allowing you to ladder your policies as desired. This feature is great if, for some reason, you need to increase your coverage. It's likewise beneficial if, for any reason, you want to decrease your coverage.

Ladder insurance is very accessible. The company writes policies in every state. The firm's partnership with Allianz Life and Fidelity Security Life enables it to do so

Ladder's No Medical Exam Policy

What's more, the company tries to avoid requiring medical exams. However, it's impossible to know whether you'll need one to qualify until you've completed the application.

Ladder life is an insure-tech company. The no medical exam policy is common in this industry. Resultantly, insure-tech companies enable many people to secure policies without the need to see a doctor.

In most instances, there's no need to submit to a blood or urine test. Instead, Ladder uses third-party data sources.

These information sources might include your prescription drug history, for example. The company will use this information to assess your risk level.

Using this practice, Ladder has reduced the number of people who require an in-person exam greatly. By using home lab kits, the company has succeeded in this mission.

However, the highest risk applicants may still find that they must submit to a doctor's visit.

Ladder Life Insurance Drawbacks

The biggest shortcoming of Ladder life insurance is that the company does not offer whole life insurance vs universal life insurance. Instead, they only offer term life insurance.

In some cases, Whole Life Vs Universal Life 004923132 (aol.com) life coverage can better meet your needs. Unfortunately, if you fit in this category, you'll have to look elsewhere for quality coverage.

Also, Ladder life insurance doesn't accept applications from adults over the age of 70. In addition, you can't purchase a policy that covers you past that age.

Imagine, for instance, that a 58-year-old consumer wants to purchase a Ladder policy. In that case, they can only apply for up to 10 years of coverage.

Also, it's common for insure-tech providers only to offer term life coverage. However, Ladder also doesn't offer riders€”limiting your options.

For instance, most insurers offer an accidental death rider. This kind of rider offers additional compensation if you should pass in an accident.

You might find this kind of rider and others highly beneficial. However, you'll need to choose another company besides Ladder if you want added security.

Ladder Life Alternatives

Term Vs Whole Life Insurance 5115999 (thebalancemoney.com) products can prove confusing and complex. Sometimes, you can feel overwhelmed by all the available options. This circumstance can make it difficult to select the best life insurance plan for your needs.

When you're shopping around for life insurance, an experienced, trustworthy agent can help you navigate all your options. They'll aid you in finding the right policy for your circumstances.

At Top Whole Life Insurance Agency, we're experienced in helping clients just like you choose from among our many top-quality carriers.

We offer policies from known providers, such as Geico Life Insurance, MassMutual Life Insurance, new york life whole life insurance review of New York, and Ohio National Life Insurance. We'll work with you one on one to help you find a plan that perfectly matches what's important to you in terms of the amount of coverage, premiums, and more.

Get the Best Quotes Quickly from Top Whole Life!

Now you know more about Ladder life insurance. You've also learned about how to get help finding the right insurance policy.

The life insurance that you choose is one of the most important decisions you can make. It's a financial safety net for your family, and it provides peace of mind.

If you need life insurance, we can help.

Top Whole Life offers fast quotes on whole life insurance faqs additional benefits whole life insurance. We'll help you find the right coverage€”and at an affordable price. At Top Whole Life, we know what works best when it comes to finding the perfect policy for your needs.

No one wants to spend hours researching different policies€”give us a call or fill out our quick form, and we'll do all the work.

Contact Top Whole Life today at (855) 946-5353 or connect with us online for a whole life quote.