Is Life Insurance Tax Deductible? Exploring the Tax Benefits of Life Insurance

Life insurance is a crucial component of comprehensive financial planning, offering protection and security for individuals and their loved ones. While the tax implications of life insurance play a significant role in shaping financial decisions, the question of whether life insurance premiums are tax deductible often arises. In this detailed exploration of the tax benefits of life insurance, we will unravel the complexities surrounding this topic that "is life insurance tax deductible€? and shed light on the various tax advantages associated with life insurance policies.

The Non-Deductibility of Life Insurance Premiums

In general, life insurance premiums are considered personal expenses and, therefore, are not tax deductible. The Internal Revenue Service (IRS) regards these premiums similarly to other personal purchases, such as a car or a cell phone, and does not provide tax deductions for them. Additionally, there is no federal or state mandate requiring the purchase of life insurance, unlike health insurance, which further reinforces the non-deductibility of life insurance premiums

Tax Benefits of Life Insurance Policies

1. Tax-Free Death Benefits

Proceeds from a life insurance death benefit are typically tax-free, providing financial protection for beneficiaries without incurring income tax implications. The tax-free nature of death benefit payouts offers invaluable security for families during challenging times.

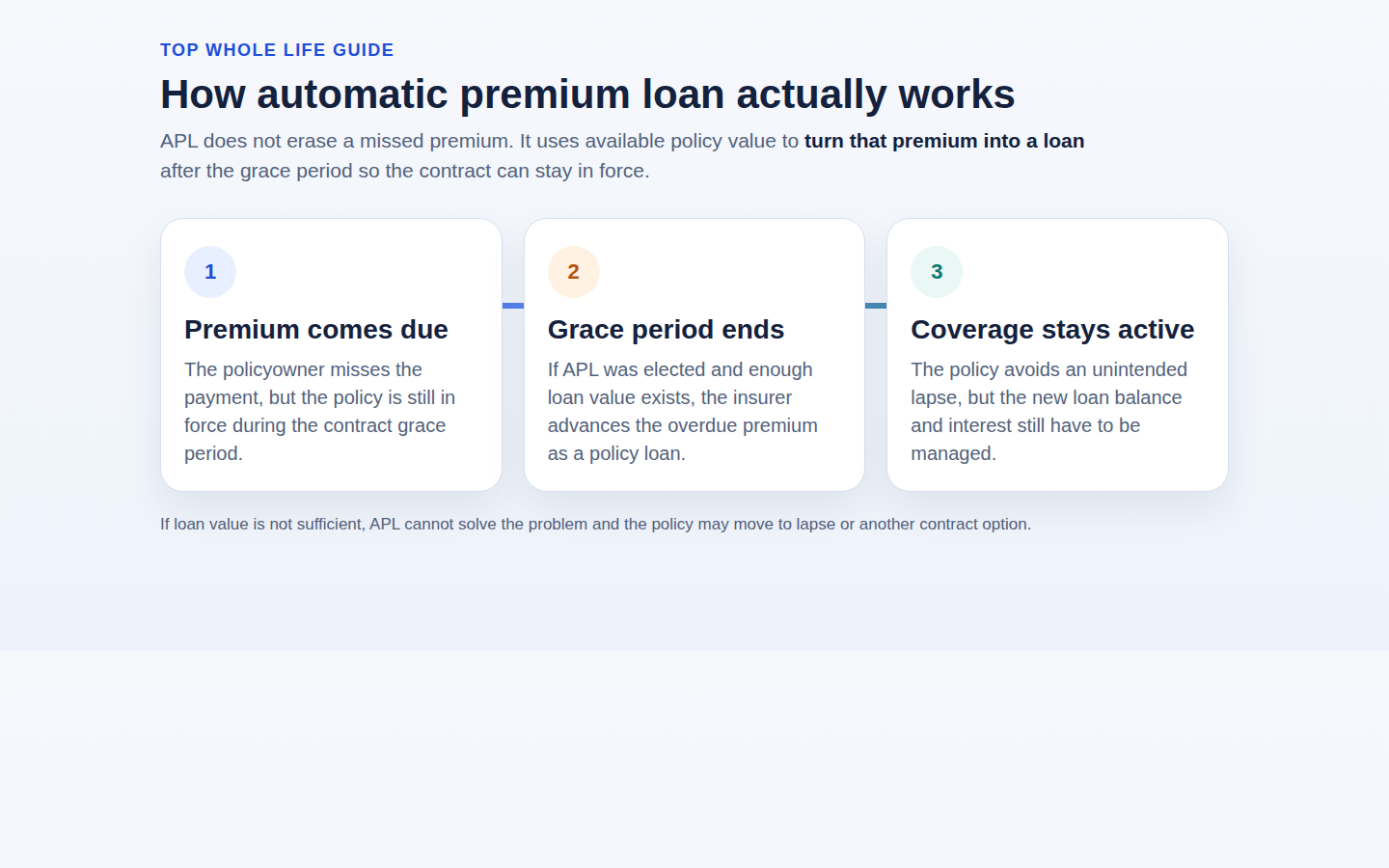

2. Cash Value Accumulation

Permanent life insurance policies, such as whole life insurance, boast the advantage of building cash value over time. This cash value accumulation occurs in a tax-advantaged manner, allowing policyholders to leverage this asset for various financial needs while enjoying tax-deferred growth.

3. Tax-Free Dividends

Cash dividends received from a life insurance policy are generally tax-free, as they are considered a return of policy premiums. This tax-free status holds as long as the dividends do not exceed the net premiums paid on the policy, offering an additional financial benefit for policyholders. Secure your future with tax-deductible life insurance today! Click below to get a Quote Now!

Managing Cash Value and Tax Implications

1. Utilization of Cash Value

Each method of utilizing a life insurance policy's cash value carries specific tax consequences and considerations. Surrenders, withdrawals, and loans against a policy have varying tax implications, and it is essential for policyholders to comprehend the potential tax outcomes associated with each method.

2. Tax-Deferred Growth

The cash value component of permanent life insurance policies offers tax-deferred growth, providing policyholders with a means of accumulating funds in a tax-efficient manner. Understanding the tax implications of cash value growth is crucial for informed financial decision-making.

Exceptions to Non-Deductibility

1. Business-Paid Premiums

Business owners can deduct premiums paid for life insurance policies owned by company executives and employees, provided that the executive or employee reports the premium as income. This exception allows for tax advantages in a business context, offering additional financial benefits for employers and employees alike.

2. Charitable Donations

Transferring ownership of a life insurance policy to a charitable organization can result in tax benefits. Both the premiums paid into the policy and those paid after the transfer may be tax deductible, presenting an avenue for charitable contributions with potential tax advantages.

Conclusion

In summary, whole life insurance premiums are generally not tax deductible, the array of tax benefits associated with life insurance policies underscores their significance in long-term financial planning and security. From tax-free death benefits to tax-advantaged cash value accumulation, life insurance offers a range of financial advantages that can complement an individual's overall financial strategy.