AARP Life Insurance Review (2026)

Updated June 19, 2026

Quick take: AARP life insurance is not issued by AARP itself — policies are underwritten by New York Life for AARP members, generally ages 50+. Strengths include simplified issue (no medical exam on many products) and brand trust; trade-offs include membership required, rising term premiums in five-year bands, and lower online coverage caps than phone applications.

What life insurance company does AARP use?

AARP partners with New York Life Insurance Company for its life insurance program. You must be an AARP member (or eligible spouse) to apply; membership is separate from the policy premium.

What Is AARP Life Insurance?

The AARP insurance program features term and permanent life insurance policies issued by New York Life. Coverage is designed for adults 50 and older, with simplified health questions instead of a full medical exam on many products.

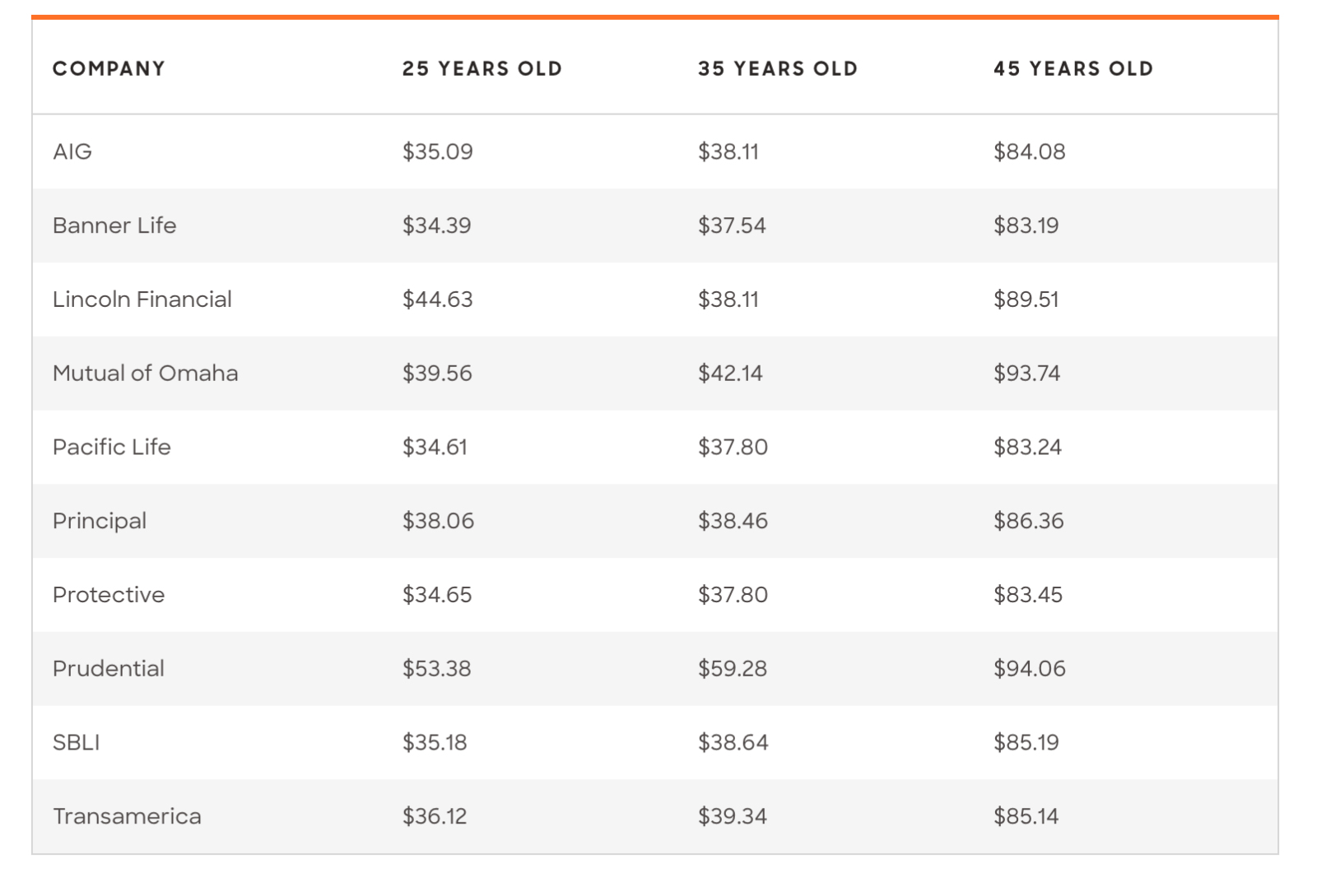

AARP Life Insurance Options Compared

Per AARP's official life insurance benefits page, the program offers three main products:

| Product | Member ages | Coverage (per AARP) | Medical exam | Premium pattern | Cash value |

|---|---|---|---|---|---|

| Term life | 50–74 (spouse 45–74) | Up to $150,000; coverage ends at age 80 | Health questions only | Increases every 5-year age band | No |

| Permanent (whole) life | 50–80 (spouse 45–80) | Up to $100,000 | Health questions only | Level for life | Yes |

| Guaranteed acceptance whole life | 50–80 (spouse 45–80) | Up to $30,000 | None (guaranteed issue) | Level for life | Yes |

AARP membership is required before applying. Standard annual membership starts at $16/year for ages 50+ (AARP membership); membership fee is separate from policy premiums.

Online applications may offer lower maximum face amounts than phone applications — contact New York Life for limits above the online cap.

Term Life Insurance

AARP members ages 50–74 can apply; spouses 45–74 may also qualify. Term coverage lasts until the policyholder's 80th birthday.

The death benefit stays level, but premiums typically increase every five years as you move into a new age band — costs are not guaranteed in advance.

Coverage is available up to $150,000 per AARP program materials; higher amounts may require contacting New York Life directly.

How Does Term Life Work?

Term life pays the selected benefit to your beneficiary when you pass away. There is no cash value; premiums are lower than permanent insurance at younger ages within the term.

Whole Life Insurance

AARP members 50–80 (spouses 45–80) can apply for whole life insurance. Premiums stay level for life, and the policy builds cash value over time.

Permanent coverage is available up to $100,000 per AARP; acceptance depends on health question responses.

How Does Whole Life Work?

Whole life includes a death benefit plus a savings component (cash value) that grows on a tax-deferred basis. You may be able to take a policy loan or withdrawal against cash value, subject to policy terms.

Guaranteed Acceptance Whole Life

Members 50–80 (spouses 45–80) can apply for guaranteed acceptance whole life. Acceptance is guaranteed except for terminal illness.

If death occurs within the first two years from non-accidental causes, only a limited benefit may be paid. Coverage is available up to $30,000 per AARP program materials.

Whole Life for Children

AARP members can buy coverage for children or grandchildren under 18 through the Young Start program — up to $20,000, no exam. The adult is beneficiary until the child turns 21 and becomes policy owner.

Life Insurance Buying Guide

Before comparing carriers, decide term vs. permanent coverage, coverage amount, and whether you need life insurance riders.

When comparing quotes, match the same death benefit and policy type. If you want to skip a medical exam, confirm simplified-issue availability.

For a deeper cost comparison, see our guide on whether AARP life insurance is worth it and AARP / New York Life coverage options.

Life Insurance Rate Factors

Rates depend on age, health, and product type. Underwriting may consider:

- HIV or AIDS diagnosis

- Asthma, diabetes, stroke history

- DUI/DWI driving record

- Drug or alcohol treatment in the past five years

- Tobacco or nicotine use in the past twelve months

AARP Insurance Riders

Accelerated Benefit

If a permanent policyholder is terminally ill (generally two-year life expectancy; one year in New York), up to 50% of the death benefit may be accessed while living.

Waiver of Premium

Permanent policyholders confined to a skilled nursing home for 180 consecutive days may qualify for premium waiver (included on permanent products in many states).

AARP Customer Satisfaction

The NAIC (National Association of Insurance Commissioners) publishes complaint ratios by company. A score of 1.0 is average. New York Life (AARP's underwriter) has historically reported below-average complaint ratios versus the industry — check the latest NAIC complaint index for current figures.

AARP Financial Strength

Policies are underwritten by New York Life, which carries top-tier financial strength ratings from major rating agencies (A.M. Best, Moody's, S&P). New York Life has ranked strongly in J.D. Power U.S. Life Insurance studies in recent years.

AARP Pros and Cons

Pros

- No medical exam on many products (health questions only)

- New York Life financial strength

- Level premiums on whole life; guaranteed acceptance option

- Low AARP membership cost ($16/year for standard membership)

Cons

- Term premiums increase in five-year age bands

- Online coverage limits; higher amounts require a phone call

- Must join AARP before applying

- Cash value growth is modest vs. dedicated investment vehicles

Is AARP life insurance worth it?

For a shorter value-focused take — premiums, coverage caps, and who should (or shouldn't) buy — see Is AARP Life Insurance Worth It?.

AARP Life Insurance Coverage — Next Steps

If you want whole life with stronger long-term cash value, compare top whole life companies for cash value before committing to AARP's simplified-issue products.

To compare AARP against other carriers for your age and health, contact us for a free, no-obligation quote.